Being Fully Invested Is Not a Virtue

The cost of holding cash appears in every attribution report. The benefit does not. That asymmetry is not an argument against cash. It is the discipline itself.

10 min read | By the team at Banyantree Investment Group

The door requires a decision before it opens: what is held here, on what terms, and when it moves. Bank vault guard, c. 1938. Library of Congress Prints and Photographs Division. Cropped, redrawn, and colour-treated.

───

Eight days after Lehman Brothers filed for bankruptcy, Goldman Sachs placed a call to Omaha.

The investment bank needed capital. Markets had seized. The terms available at that moment were available only to someone who could write a cheque large enough to matter, immediately, without first becoming a seller. Warren Buffett had been preparing for a call like this for two years without knowing it would come. Berkshire Hathaway was sitting on more than forty billion dollars in cash and Treasury bills, a figure that had attracted regular commentary in the financial press, none of it flattering. The market had spent five years advancing. Private equity firms were buying entire companies with borrowed money and generating returns that made Berkshire’s look pedestrian. A generation of investors had concluded, reasonably, that the old man from Omaha had been left behind by a world that moved faster than he did.

The question at every shareholder meeting, in every research note, in every investment conference hallway, was the same: what is he waiting for?

The answer arrived on 23 September 2008. Ten per cent per annum on five billion dollars in preferred shares, plus warrants on a further five billion in common stock at a fixed price. Buffett later noted, with evident satisfaction, that the arrangement was producing roughly $1.4 million a day. The cash pile that had looked lazy was not laziness. It was the funding instrument for terms available only to someone who had spent years enduring the charge that they were not doing enough with their money.

───

Seth Klarman reached the same conclusion through different reasoning, and with fewer dramatic moments to show for it.

Through 2006 and 2007, as credit spreads compressed and equity markets advanced, his Baupost Group held between forty and fifty per cent of its assets in cash. Clients wrote. Consultants expressed concern. The fund’s relative performance, measured against benchmarks that were fully invested and rising, was uncomfortable. Many funds holding large cash positions in those years were making a forecast: that the market would fall, and soon. Klarman was making something different. He was making a pricing judgement. The available alternatives, at prevailing prices, did not clear his hurdle. Nothing about that judgement required knowing when markets would correct. It required only an honest assessment of what was on offer.

When the crisis arrived, the criticism stopped. Through 2008 and into 2009, Baupost deployed its reserves into distressed debt that had fallen to fractions of face value. CIT Group bonds bought at sixty-five cents on the dollar yielded fifteen per cent and later converted into securities worth eighty cents. The discomfort of the preceding two years had not been an error. It had been the price of admission.

That distinction, between a pricing judgement and a forecast, is where the argument lives. Market timing is a prediction: the view that the market will fall, probably soon, and that being out of it is therefore wise. Holding cash as a pricing judgement is not that. It is the assessment that the current opportunity set does not compensate adequately for the risk that must be accepted to own it. One statement requires a prediction about prices. The other requires only a view about value. The difference is the difference between a forecast and a discipline.

───

There is an asymmetry in how cash is judged that shapes every conversation investment committees have about it.

When cash lags a rising market, the accountability is immediate. The attribution report shows the drag. The consultant’s question arrives in the next quarterly review, politely phrased and unmistakably pointed: why are we paying fees for this? The manager must answer, specifically, in writing, for the visible cost of patience.

When a fully invested portfolio falls alongside the market, the conversation is different in kind. The language shifts. Markets were down broadly. The strategy behaved as expected in a difficult environment. We stayed the course. The loss is shared across the industry, and what is shared is absorbed differently from what is singular. Nobody writes a pointed letter demanding to know why the manager owned what the index owned when the index fell thirty per cent.

Consider two managers. The first holds fifteen per cent cash through a strong market and lags the benchmark by a hundred and twenty basis points. The second owns the benchmark through a sharp correction and loses eighteen per cent. The first faces pointed governance questions. The second faces sympathy. Yet the better decision may well have been the first one. The portfolio that fell thirty per cent was expressing a view: that the opportunity cost of cash exceeded the risk of full deployment. That view simply concealed its assumptions more effectively, because it dressed itself in the appearance of action.

Being fully invested is not a virtue. It is a choice, and a choice with costs that are real but deferred.

───

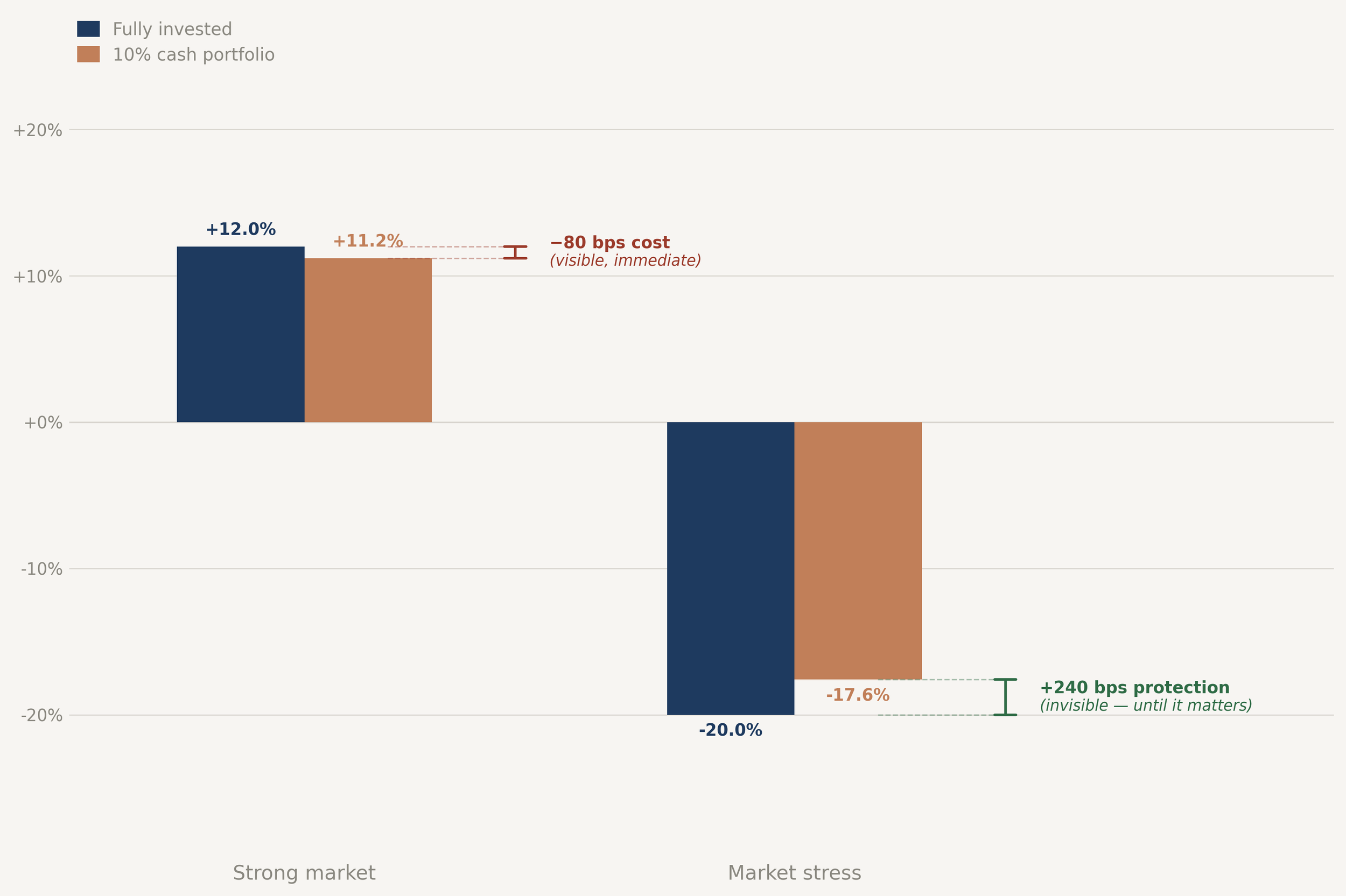

Cash has a cost. The premium it exacts is real and should be acknowledged without flinching: the foregone return of not owning the next-best alternative, plus whatever purchasing power inflation erodes. In a portfolio holding ten per cent in cash at four per cent, against a risk asset returning twelve per cent, the drag for the year is approximately eighty basis points. That number belongs in every committee discussion that raises the subject.

The cost shows up in every attribution report. The benefit does not. If the same risk asset falls twenty per cent, the portfolio with cash avoids two percentage points of loss. More than that, it retains the capacity to act: to buy more of the same asset at lower prices, or to take advantage of dislocations elsewhere, without first needing to raise liquidity by selling something else at a loss. In March 2020, high-quality bonds were sold as investors scrambled for cash. Treasury markets, the closest thing to cash itself, became difficult to transact at reasonable prices. Actual cash required no buyer. It was simply available, without condition, at the moment when availability was the only thing that mattered.

The question is not whether cash outperforms. It is whether the option to act, valued honestly, is worth the premium paid to hold it. When alternatives offer generous compensation for their downside, when entry terms are compelling and the dispersion of outcomes is narrow, the option is worth less. Own the assets. When alternatives offer thin compensation for wide uncertainty, when crowded positioning makes exits unreliable and correlations are likely to rise under stress, the option becomes more valuable. Hold cash. The judgement sits between those two states, and it moves.

───

Exhibit 1 : The Opportunity Cost, Both Sides of the Ledger

Illustrative. Risk asset: +12% in strong market, −20% in stress. Cash at 4% per annum. Portfolio holds 10% cash. Not personal advice.

Cash is a position when uncertainty is not compensated. That is a pricing judgement, not a forecast.

───

The failure mode most common in practice is not holding too much cash. It is holding cash without a reason.

When cash accumulates because the investment process has stalled, or because the committee cannot reach a decision, it is not a position. It is a symptom. It cannot survive scrutiny because there is nothing to scrutinise. Cash held because alternatives do not clear a stated hurdle, because liquidity has option value in a specific environment, because the entry terms for available assets are genuinely unattractive: that is auditable and defensible. The difference between them is not the cash weight. It is whether the reasoning exists before the outcome is known.

The same logic governs the exit. A cash position that cannot name the conditions under which it would be reduced is not a position. It is a mood.

Patience without triggers is procrastination. Patience with triggers is process.

A position that moves between five and fifteen per cent in response to the quality of the opportunity set stays inside portfolio construction. A decision to move from fully invested to entirely in cash is almost always a macro call, regardless of how it is framed. The cash dial works. The cash switch becomes an oracle.

───

What would change this view?

Here is the more uncomfortable version of this discussion.

The decade from 2009 to 2019 came close to breaking the framework. Central banks in most major economies compressed cash yields to near zero, and in some jurisdictions below it. A manager running five to fifteen per cent cash through those years was not paying a modest premium for the right to act at better prices. They were paying a substantial and compounding real cost for opportunities that, in many cases, never arrived at materially lower prices than those available in 2010, 2012, or 2015. Assets that looked inadequately compensating for their risk compounded at double digits. The cash generated nothing. Investors who held cash patiently through that cycle did not collect a payoff. They collected the premium cost, repeatedly, without a corresponding benefit.

This is not a hypothetical inconvenience. It is a decade of actual results. The framework requires an opportunity set in which the option periodically pays off, in which better entry points materialise often enough to justify the drag. For a sustained period, that condition did not hold. A manager who held fifteen per cent cash from 2010 to 2019 and points only to 2008 as vindication is making a selective argument.

The second challenge is inflationary. At the levels seen across Australia and most developed markets in 2022 and 2023, a ten per cent cash position was losing purchasing power at six to seven per cent annually. The framework treats cash as capital-preserving between deployment decisions. In a sustained inflationary regime, that assumption weakens, and the cost of patience compounds in a way the simple opportunity-cost arithmetic does not fully capture.

The third challenge is substitution. The strongest claim for cash is its unconditional availability. It does not require a buyer, it does not depend on market depth, it is simply there. If downside protection could be bought consistently, cheaply, and with enough reliability to replicate that optionality at a lower carrying cost, the case for holding cash specifically would weaken. That has not happened in a durable way. Protection tends to become expensive precisely when it is most needed. Still, it is a serious question, and one worth pressing.

The rate and inflation backdrop is less hostile to cash than it was. The case for a cheaper, reliable substitute still has not been proved. A manager holding cash as a principled position should be able to answer, specifically: what level of cash yield, what inflation rate, what length of underperformance, and what credible alternative source of optionality would cause them to reconsider. If the answer is vague, the discipline may be less rigorous than the language suggests.

───

In the years after the 2008 crisis, the portfolios that had held cash did not merely avoid losses. Berkshire ultimately made roughly $3.7 billion from the Goldman investment alone: the preferred dividends, the redemption premium, and the gain on the warrants. The CIT Group bonds Klarman had bought at sixty-five cents converted into securities worth eighty cents. These were not the outcomes of prescient forecasting. They were the outcomes of having capacity when capacity was scarce, of having spent years paying the premium on an option that almost everyone else had allowed to expire.

The premium on that option was highest in 2006 and 2007, precisely when markets were rising and patience looked most like negligence. It was highest then because that was what the option was worth: the right to act when the conditions that made patience expensive would eventually reverse.

Cash is expensive when it is most worth having. That is not a paradox to resolve. It is the discipline itself.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative and hypothetical. This material is intended for wholesale and professional investors.