Style Neutral

Why We Don't Pick a Lane

By the team at Banyantree Investment Group

Before databases and dashboards: the slow craft of organising knowledge, one card at a time, until the system becomes searchable. Library catalogue room, c. 1917–1920. Source: Library of Congress Prints and Photographs Division. Cropped, redrawn, and colour-treated.

───

On the morning of Tuesday, 7 August 2007, something impossible began happening to some of the most sophisticated investment funds in the world.

Goldman Sachs Global Equity Opportunities, a quantitative hedge fund that used mathematical models to identify mispricings across thousands of stocks, started losing money. So did Renaissance Technologies, run by the former codebreaker Jim Simons and widely considered the most successful hedge fund in history. So did Highbridge Statistical Opportunities, and Tykhe Capital, and a dozen other funds whose names most investors had never heard. By the end of the week, Goldman's fund had lost close to a third. Highbridge was down around eighteen per cent. Renaissance reported losses of nearly nine per cent in a strategy that had rarely experienced a losing month.

The losses were not the remarkable part. Markets move; funds lose money. The remarkable part was that these funds were designed to be uncorrelated with one another. They were 'market neutral', meaning they held roughly equal long and short positions and were supposed to be insulated from broad market swings. They used proprietary models built by separate teams in separate cities, guarded with the secrecy of state intelligence services. They should not have moved together. And yet, with what one researcher later called 'laser-like precision', they all fell at once.

The S&P 500, meanwhile, barely moved on Tuesday and Wednesday. Whatever was happening was happening only to quants.

The diagnosis came later. Andrew Lo, a finance professor at MIT, reconstructed the week using transaction data and simulated portfolios. His conclusion was simple and unsettling: the funds had independently discovered similar opportunities. They had converged, without coordinating, on overlapping positions. The same value signals. The same momentum indicators. The same factor exposures. When one large player began liquidating, probably to meet margin calls from losses elsewhere, it moved prices against everyone holding the same trades. Those price moves triggered further selling, which triggered further losses, which triggered more selling still. The cascade lasted three days. Goldman's chief financial officer, in a moment of uncharacteristic candour, described it as the crowded trade overwhelming market fundamentals.

The crowded trade had overwhelmed market fundamentals. It was not that the underlying analysis was wrong. The stocks the quants owned were still cheap by their models; the stocks they had shorted were still expensive. The thesis was intact. What failed was the assumption that each fund's exposure was its own. In reality, they had all made the same bet on a style of investing, without knowing it.

───

The word 'style' appears constantly in the investment industry. It is printed on fund prospectuses and consultant questionnaires. It organises the Morningstar grid into boxes labelled 'large value' and 'small growth'. It shapes how committees construct portfolios and how they evaluate the managers who run them.

The standard styles are familiar enough. Value means buying companies that are cheap relative to their fundamentals: low prices compared to earnings, book value, or cash flow. Growth means buying companies whose earnings are expected to expand rapidly, usually at higher valuations. Quality means buying companies with strong balance sheets, stable margins, and consistent profitability. Momentum means buying companies whose prices have recently risen, on the theory that trends persist. Low volatility means buying companies whose share prices move less than the market, often utilities and consumer staples.

Each of these styles has a body of research behind it. Fama and French documented the value premium. Jegadeesh and Titman documented momentum. Novy-Marx documented profitability. Over long horizons, these effects have been real enough to tempt almost everyone.

But the part that rarely appears in the marketing materials is also real: every one of these styles goes through extended periods of painful underperformance. Value can lag for years. Momentum can crash. Low volatility can trail badly when the rate regime shifts. The premiums exist, but they are not delivered smoothly. They arrive in bursts, separated by long stretches when believers question their faith and committees question their managers.

This is where the trouble begins. Commit to a single style and you are not merely selecting stocks. You are making a bet on when your style will be rewarded. That is a macro bet, dressed in the language of bottom-up investing.

Style-neutral positioning is a refusal to make that bet. It means selecting ideas bottom-up first, and then monitoring style and factor exposures as risks, not treating them as an identity.

───

Bill Miller's career made this tension visible.

For fifteen consecutive years, from 1991 through 2005, Miller's Legg Mason Value Trust beat the S&P 500. It was the longest streak on record. Magazine profiles appeared. Books were written. Assets poured in, eventually reaching twenty-one billion dollars. Miller became, in the estimation of the financial press, one of the greatest stock pickers of his generation.

The fund was called Value Trust. The label was in the name. But Miller's portfolio did not look like a traditional value fund. He owned Amazon when most value managers considered it uninvestable. He owned Google after its IPO. He owned financial stocks heavily, including Countrywide, AIG, and Bear Stearns, on the theory that they were misunderstood and cheap relative to the risks.

In 2008, Value Trust lost fifty-five per cent. The S&P 500 lost thirty-seven. The difference, eighteen percentage points of additional loss in a year when clients could least afford it, was enough to end the conversation. Redemptions followed. Assets fell from twenty-one billion to less than three. Miller stepped down from the fund in 2012.

What did the clients think they had bought?

The name said value. The Morningstar box said large-cap blend, then large-cap value, then something else as the style-based classification struggled to keep up with what Miller actually owned. A committee evaluating the fund against a value benchmark would have seen tracking error rising for years before the crisis. A committee evaluating it against Miller's actual approach, buying securities trading below his estimate of intrinsic value regardless of how they were labelled, would have seen something different: a concentrated portfolio of high-conviction ideas, some of which happened to be in sectors that were about to implode.

The confusion was not Miller's alone. It was structural. The industry's habit of sorting managers into style boxes creates an expectation that a ‘value’ fund will behave like value, a ‘growth’ fund like growth, and so on, that the portfolio may or may not satisfy. When the label and the portfolio diverge, the committee faces a question it may not have anticipated: which one did we actually hire? But the failures here are distinct and should not be conflated. The committee’s failure was accepting a label as a substitute for understanding the actual portfolio. Miller’s failure was allowing that misapprehension to stand, continuing to present the fund under a name and identity that no longer described what it held. Both errors were real. One is a governance problem. The other is a manager conduct problem. Style-neutral discipline addresses the first; transparency and honest mandate description address the second.

───

Style drift is the industry's term for what happens when a portfolio's characteristics migrate away from its stated label without an explicit decision to change. It is one of the most common sources of governance friction between managers and the committees that oversee them.

The pattern is predictable. A manager is hired as value. Value underperforms for two years. The pressure builds: pointed questions in quarterly reviews, consultant notes flagging 'relative performance concerns', the quiet awareness that peers who own what is working are having an easier time. The manager makes a series of small adjustments, a growth name here, a momentum tilt there, each individually defensible, none announced as a change in philosophy. Performance improves. The committee relaxes. Then the cycle turns, the adjustments that helped become the positions that hurt, and everyone discovers that the portfolio is no longer what it was supposed to be.

From the manager's perspective, the adjustments were survival. From the committee's perspective, the problem is not that the manager made money for a while. The problem is that the total portfolio, which may include other managers each selected for a role, now has exposures that nobody explicitly approved. The value allocation is no longer providing value exposure. The diversification the committee thought it had purchased has quietly evaporated.

This is why style labels, despite their administrative convenience, create governance risk. A label is a promise about how the portfolio will behave. When the portfolio stops behaving that way, the promise is broken, even if performance is strong. Drift that works is still drift.

───

The alternative is style-neutral positioning. Style-neutral does not mean ignoring styles or pretending that factor exposures do not exist. It means refusing to let a label dictate decisions.

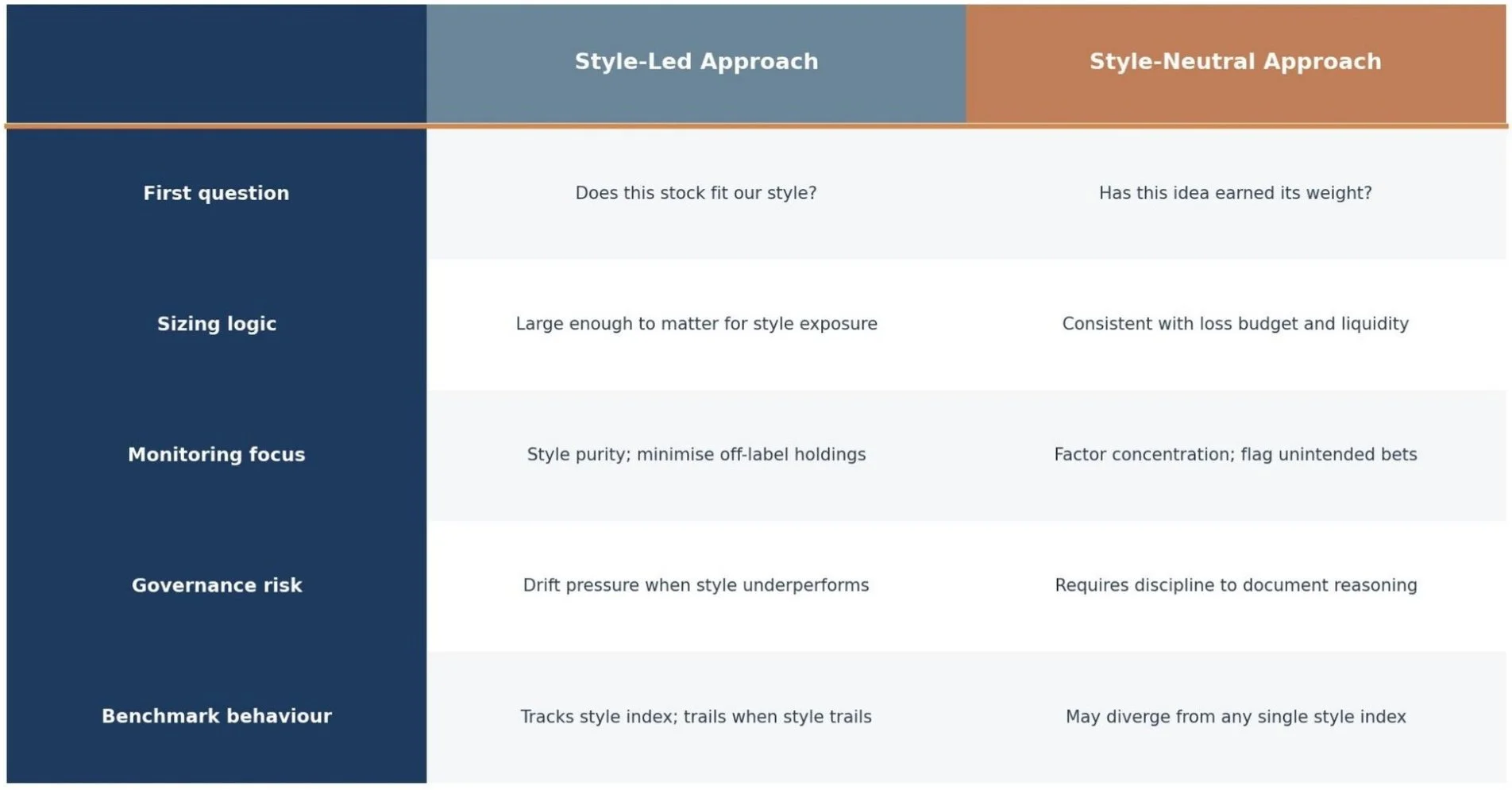

A style-neutral portfolio starts with a different question. Instead of asking, 'Which stocks fit our style?' it asks, 'Which ideas have earned their weight?' The distinction matters because the first question presupposes the answer (the style comes first, the holdings follow) while the second question lets the answer emerge from the work.

In practice, this means evaluating each opportunity on its own terms: the quality of the business, the valuation relative to a range of outcomes, balance sheet resilience, liquidity, downside risk. An idea might be cheap by traditional value metrics. Or it might be expensive by those same metrics and still compelling for other reasons. The question is not whether it fits a box. The question is whether the thesis is sound, the position can be sized safely, and the expected return compensates for the risk.

Once the holdings are selected, style exposures become a monitoring exercise rather than a design constraint. The portfolio will have some factor profile, as every portfolio does, and that profile should be measured, reported, and reviewed. The governance question is whether the profile reflects bottom-up decisions or whether it has drifted into an unintended concentration. A dominant factor bet is still a bet, even if it arrived by accident. Treat factor exposure as a risk metric, not an identity, and you can catch concentration before it becomes dangerous.

This aligns naturally with benchmark-unaware investing. Just as index weights provide context but do not dictate holdings, style labels can be monitored without becoming prescriptive. The mandate is the anchor. The benchmark is a reference point. The label is optional.

Ideas must earn weight; exposures are monitored. This is auditable in a way that style labels are not. The expectation is clear: bottom-up decisions with explicit oversight of unintended bets. The anchor is the process. The guardrail is exposure monitoring.

───

Exhibit 1. Same Portfolio, Two Questions

A style label is a comfort blanket. It can also become a substitute for thinking. The alternative is not “style-less”, but style-aware without being style-captive. Illustrative and hypothetical.

───

None of this eliminates the difficulty of looking different. A style-neutral portfolio will, by construction, trail whichever style is leading at any given moment. When value surges, the portfolio will have less value exposure than a value fund. When growth dominates, it will have less growth exposure than a growth fund. The committee will ask why the portfolio does not look more like whatever is working. The manager will explain, again, that the goal is not to maximise exposure to the current winner but to compound through the full cycle without being forced to sell at the worst time.

The explanation is correct, but it is not comfortable. Comfort comes from conformity, and style neutrality is a deliberate refusal to conform to a single factor. The discomfort is the price of avoiding the larger risk: hidden concentration, crowded trades, the next August 2007.

───

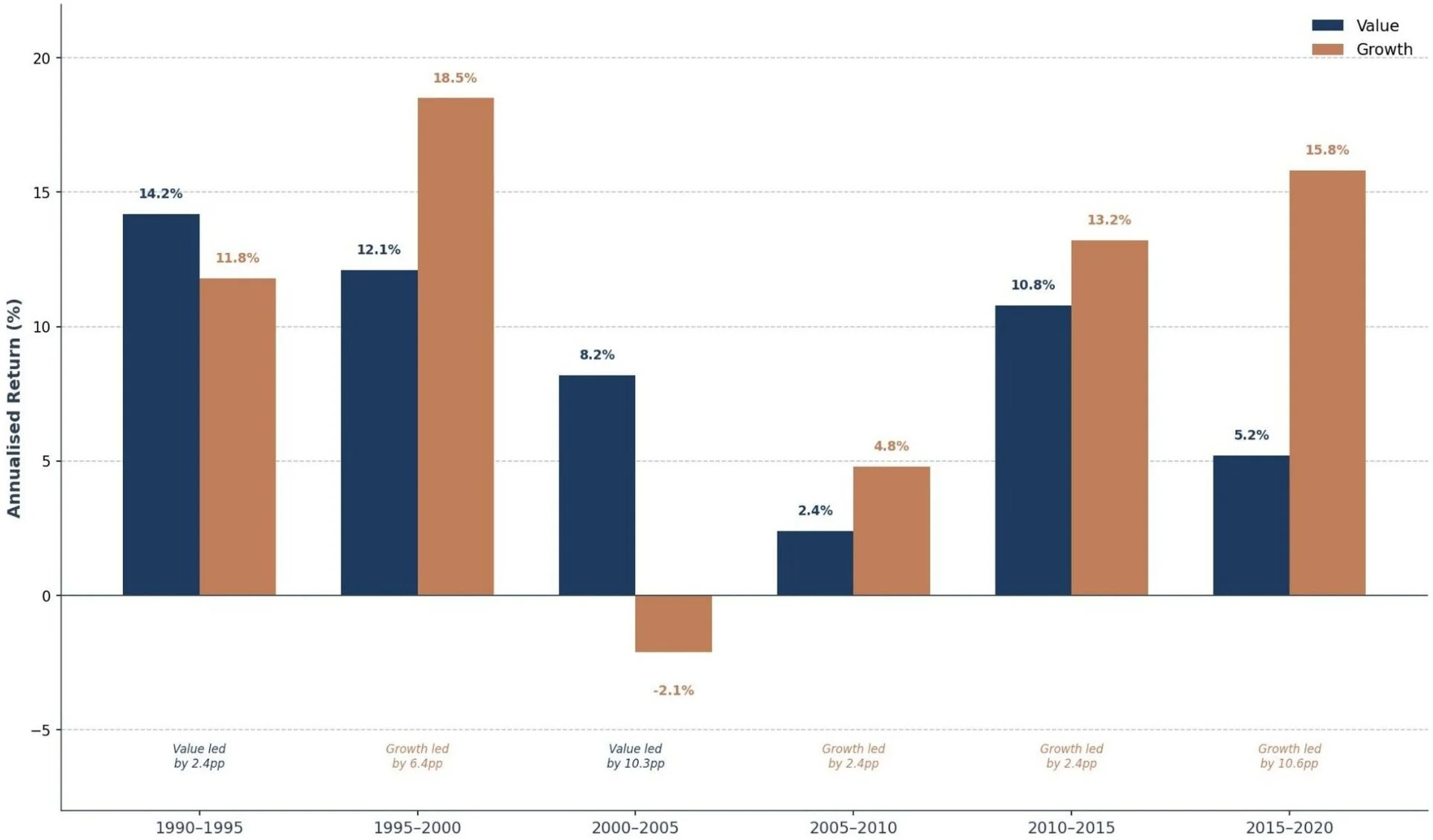

Exhibit 2. Style Leadership Rotates

The market does not crown a winner and keep the crown in place. It rotates it, often at the exact moment investors decide the last winner is “the new normal”. Illustrative and hypothetical.

───

What would change this view?

Two conditions would require genuine reconsideration.

The first is evidence that factor timing has become reliably forecastable. The best work on the subject still suggests it is tempting, and mostly unreliable. But research evolves. If a body of evidence emerged showing that rotation could be predicted with the consistency required for real-world governance, the case for maintaining factor-agnostic exposure would weaken. The portfolio could instead tilt dynamically toward whichever factor was about to lead. That is not the world we observe today, but it is a testable claim, and if the evidence changed, the conclusion should change with it.

The second is a structural shift in passive investing that makes style neutrality untenable. The growth of index funds and 'smart beta' products means that large pools of capital now flow mechanically into factor-defined strategies. If those flows became large enough and persistent enough to make certain factor exposures self-reinforcing, to the point where underweighting them carried structural rather than merely cyclical risk, then a style-neutral approach might leave permanent return on the table. This is a live debate. Anyone who has watched mega-cap concentration compound for years has grounds to press on it.

Neither condition holds in the form that would overturn the framework. Both deserve monitoring.

───

The quants who lost money in August 2007 were, by any reasonable measure, among the smartest investors in the world. They had built systems that identified mispricings invisible to the human eye, exploited them with precision, and compounded returns for years. What they had not built was a system for knowing when everyone else had discovered the same thing.

That is the deepest argument for style neutrality. It is not that styles lack merit; the research is real, the premiums exist. It is that a style, once adopted, becomes a position in a trade that may be more crowded than it appears. The label that simplifies marketing complicates governance. The box that organises the consultant's report can hide the exposures that matter most.

A portfolio that refuses to pick a lane requires a longer conversation, a clearer process, and discipline in execution. The benefit is a portfolio that can survive contact with a market that does not care about labels, one that compounds through the full cycle because it was never imprisoned by a style that happened to be out of favour.

Pick ideas, not lanes. Then watch your lane markers.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative and hypothetical. This material is intended for wholesale and professional investors.