The Barbell

Core Holdings and High-Conviction Ideas

By the team at Banyantree Investment Group

A reminder that measurement came before opinion: weight, counterweight, and the discipline of proving what something is worth. Byzantine steelyard balance, 5th–7th century CE. The Metropolitan Museum of Art, New York. Cropped, redrawn, and colour-treated.

───

On the morning of 7 April 2020, Mark Spitznagel sent a letter to the clients of Universa Investments. The number at the top of the page was difficult to process: a return of 4,144 per cent for the first quarter. Two weeks earlier, the S&P 500 had completed its fastest descent into a bear market in history. The index fell thirty-four per cent in twenty-three trading days. Liquidity vanished. Correlations spiked toward one. Portfolios that had appeared diversified revealed themselves to be variations on the same trade. And Universa, a fund that had been losing small amounts for years while the market climbed, had just delivered returns so extreme they looked like typographical errors.

Spitznagel's strategy was not complicated to describe. Universa held deeply out-of-the-money put options, instruments that would expire worthless in calm markets but explode in value during a crash. The fund paid a small premium, quarter after quarter, for the right to profit from catastrophe. It was, in Spitznagel's words, 'the most bearish expression of the market there is'. And yet his clients did not use it to bet against equities. They used it to stay invested in them.

The arithmetic was counterintuitive but precise. A portfolio with just 3.3 per cent allocated to Universa and the remaining 96.7 per cent in the S&P 500 would have been unscathed in March 2020, a month when the equity benchmark fell more than twelve per cent. The small allocation to the asymmetric position had absorbed the entire drawdown. Over the decade through early 2020, that same combination had compounded at 12.3 per cent annually, outperforming both the index alone and portfolios hedged with bonds or gold.

The structure had a name. Nassim Nicholas Taleb, the mathematician and philosopher who served as Universa's scientific adviser, had introduced it years earlier in his book Antifragile. He called it the barbell.

───

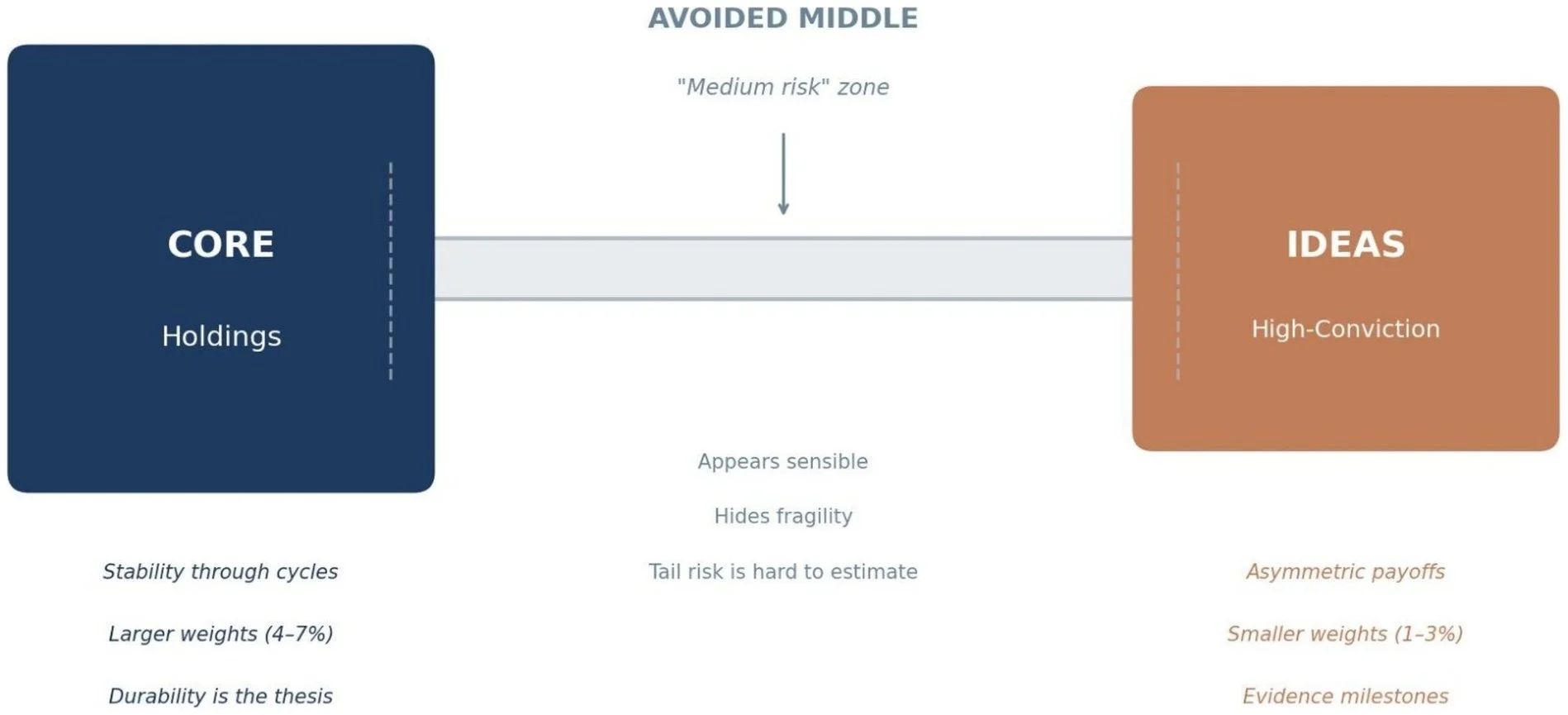

The barbell is not a portfolio allocation. It is a design principle.

In Taleb's formulation, the barbell consists of two extremes with nothing in the middle. On one end sits extreme safety: assets or positions designed to survive a wide range of outcomes, including outcomes you cannot forecast. On the other end sits extreme opportunity: positions with asymmetric payoffs, where the upside is large relative to the downside you are willing to accept. What you avoid is the middle, the zone of 'medium risk' that appears sensible but hides fragility.

The logic is not about optimism or pessimism. It is about the limits of knowledge. Taleb's argument, developed across several books, is that risks at the tails of a distribution are inherently difficult to estimate. A portfolio constructed entirely of medium-risk positions is exposed to errors in those estimates. If the model is wrong, the portfolio can be ruined. A barbell clips the downside by design. The safe portion cannot lose more than its modest expected return. The speculative portion can lose only what you allocated to it. The combination creates what Taleb calls antifragility: a structure that benefits from volatility rather than being destroyed by it.

'For antifragility is the combination aggressiveness plus paranoia,' Taleb wrote. 'Clip your downside, protect yourself from extreme harm, and let the upside, the positive Black Swans, take care of itself.'

The application to portfolios is direct. A durable core provides the stability that allows you to hold through stress. A smaller allocation to high-conviction ideas provides the asymmetry that can make a material difference when you are right. Neither component works in isolation. The core without the ideas becomes an expensive form of comfort, compounding slowly while the world changes around it. The ideas without the core become a collection of concentrated bets with no margin for error. The barbell is the structure that allows both to coexist.

───

Exhibit 1. The Barbell Structure

The middle is where portfolios go to feel responsible. It is also where hidden fragility tends to live. The barbell is a refusal to confuse “reasonable” with “robust”. Illustrative and hypothetical.

───

Stanley Druckenmiller built one of the most remarkable track records in the history of professional investing: thirty years of compounding at more than thirty per cent annually, with no losing years. His philosophy sounds reckless until you examine it closely.

'Put all your eggs in one basket,' he liked to say, quoting Mark Twain, 'and watch the basket very carefully.'

What Druckenmiller meant was not that diversification is foolish. He meant that conviction, when it is genuine, should be expressed with size. 'The mistake I'd say ninety-eight per cent of money managers and individuals make is they feel like they've got to be playing with a bunch of stuff,' he said in an interview. 'If you really see it, put all your eggs in one basket and then watch the basket very carefully.'

He pointed to Warren Buffett, Carl Icahn, and George Soros as examples. 'They all only have one thing in common. And it's the exact opposite of what they teach in business school. It is to make large concentrated bets where they have a lot of conviction.'

The key word is conviction, and its meaning is often misunderstood. For Druckenmiller, conviction was not a feeling. It was a description of work. A position earned conviction through research, through evidence, through a thesis that could be articulated and tested. Once conviction was established, the size followed. His mentor Soros had taught him to 'go for the jugular' when the opportunity was clear. In 1992, when Druckenmiller proposed shorting the British pound with one hundred per cent of the Quantum Fund, Soros responded with disdain. The opportunity, he said, was good enough to short two hundred per cent. The trade netted more than a billion dollars in a single day.

But Druckenmiller also provided the cautionary tale. In January 2000, after riding the technology boom with discipline and selling his positions at what he judged to be the right time, he watched two internal portfolio managers continue to make money in stocks he had exited. 'I just couldn't stand it anymore,' he recalled. 'For two days, I'm ready to pick up the phone and buy this stuff back. I pick up the phone and I buy them. I might have missed the top of the Dotcom Bubble by an hour.' He lost three billion dollars on that trade alone.

The lesson was not about technology stocks. It was about structure. Druckenmiller had built a portfolio that could survive his own discipline. Then he abandoned the discipline. 'I already knew better,' he said afterward. The barbell had worked. The problem was not the design. It was the decision to override it.

───

In practice, the barbell translates into two questions that most portfolios never explicitly answer.

The first question is: what must be safe?

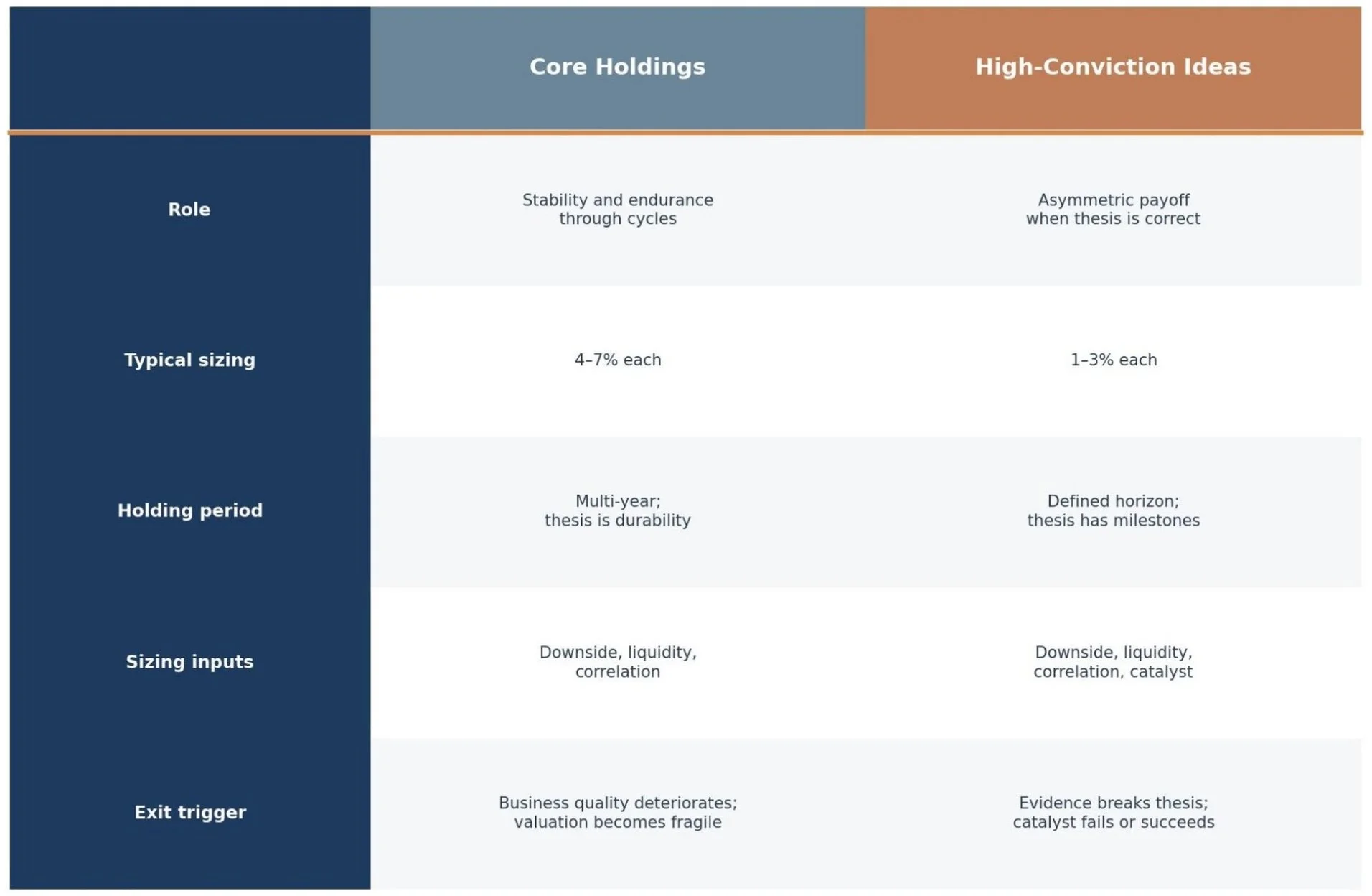

A core holding is not simply a large position or a familiar name. It is a position designed to be held through cycles, one whose role is durability rather than excitement. The characteristics are specific. Resilient economics across a range of environments, not just the environment of the last decade. Balance sheet strength and acceptable funding risk. Business quality that reduces the probability of permanent impairment. Liquidity adequate for the mandate and position size. Valuation that does not rely on perfection.

Core does not mean 'never sell'. It means 'do not buy something you cannot sensibly hold'. The test is whether the position can remain in the portfolio through a drawdown without forcing a decision you would not want to make. If the answer is no, it is not core. It is something else wearing the label.

The second question is: what is allowed to be opportunistic?

A high-conviction idea is not a risky stock. It is a position where the research work is unusually deep or differentiated, where the thesis has specific evidence milestones, where there is a plausible path to an asymmetric payoff, and where the downside is understood and sized accordingly.

The word 'conviction' should describe the quality of the work and the clarity of the thesis, not the amount of risk being taken. Risk is controlled by sizing. Conviction is expressed through research.

This distinction matters because 'high conviction' is one of the most abused phrases in professional investing. It gets used to justify oversized positions, to explain why a portfolio looks different from its peers, to provide a narrative for concentration that may or may not have been deliberate. A discipline requires a sharper definition. A position earns the label 'high conviction' when it meets specific criteria, documented before the outcome is known. It keeps the label only as long as those criteria remain intact.

The barbell, in this sense, is how risk-first thinking manifests in portfolio structure. The principle that downside sets size applies to both ends of the barbell. Core and ideas are sized using the same logic: downside, liquidity, and correlation. What differs is the typical range and the holding period, not the discipline.

───

Exhibit 2. Two Buckets, One Risk Budget

Not every holding deserves the same kind of patience. Some earn longevity through durability; others earn a place through asymmetry, and keep it only by meeting milestones. Illustrative and hypothetical.

───

The barbell fails in predictable ways, and most of the failures involve confusion about roles.

The first failure is calling concentration 'high conviction' without sizing discipline. A portfolio manager who has done deep work on a business may believe, correctly, that the thesis is strong. The temptation is to size the position to match the strength of the belief. But conviction about the thesis is not the same as certainty about the outcome. Sizing must still reflect downside, liquidity, and correlation with other holdings. A position can be high conviction and still be capped at two per cent because the downside in a stress scenario is forty per cent and the portfolio's loss budget cannot accommodate more.

The second failure is a core that is not actually durable. A collection of popular, highly valued names can look like a core in calm markets and behave like a leveraged bet in stress. Durability must be tested, not assumed. If the core is crowded, or priced for perfection, or dependent on a single narrative, it may provide no stability when stability is needed most.

The third failure is ideas that are really theme baskets. Multiple positions can look diversified by name but express the same underlying trade. Three 'ideas' in different companies that all depend on the same interest rate trajectory, or the same commodity price, or the same regulatory outcome, are not three ideas. They are one idea wearing three costumes. This is how hidden concentration forms, and it is why factor and theme exposure must be monitored across the ideas bucket, not just within individual positions.

The fourth failure is the absence of pre-commitment. Without explicit rules for when to trim and when to exit, ideas become permanent residents. The barbell dissolves into a muddle of positions that were once opportunistic and have since become simply held. Pre-commitment means writing down, before the position is taken, what evidence would confirm the thesis, what evidence would break it, and what price or valuation move would trigger resizing. Pre-commitment makes the process auditable rather than improvisational.

───

What would change this view?

Three conditions would require genuine reconsideration.

The first is a correlation regime shift that causes core holdings to stop providing stability. The barbell depends on the core behaving differently from the ideas in stress. If correlations rise permanently, so that even durable businesses fall alongside speculative ones in a crisis, the structure loses its protective value. This happened briefly in March 2020, when even Treasury markets became difficult to transact. It resolved within weeks. A regime where it did not resolve would require a different design.

The second is a liquidity environment that prevents ideas from being resized. The barbell requires the ability to act. If markets become so illiquid that positions cannot be trimmed without unacceptable cost, the ideas bucket must shrink, regardless of the quality of the theses within it. Liquidity is not a background condition. It is a binding constraint, and the barbell must adapt to it.

The third is evidence that 'medium risk' consistently outperforms. Taleb's framework assumes that the middle of the distribution is where danger hides, that moderate positions carry tail risks that are difficult to estimate and easy to underestimate. If a body of evidence emerged showing that medium-risk portfolios reliably compound better than barbells over full cycles, the framework would need revision. That evidence does not exist in the form that would overturn the conclusion. But it is a testable claim, and claims should be tested.

───

A barbell can appear inconsistent. Stable holdings on one side, more aggressive positions on the other. Which one is the portfolio?

The answer is that consistency lives in the structure, not in the individual positions. The core is there to provide stability, to prevent forced selling, to allow the portfolio to remain invested through drawdowns. The ideas are there to express the best research, to capture asymmetric payoffs, to move the needle when the work is right. Different roles, different sizing rules, one risk budget.

The barbell is not a personality. It is a design. It answers, before the market forces the question, what must be safe and what is allowed to be opportunistic. It makes the trade-off explicit, so that neither the committee nor the manager is surprised when the portfolio behaves exactly as it was built to behave. The precise ratio of core to ideas is not fixed; it is mandate-specific, governed by the loss budget described in the risk-first framework, and calibrated to what the portfolio must survive before it can compound. How those bands are set, maintained, and reviewed in practice is the subject of the portfolio construction work that follows from this principle.

Build the core to endure. Size the ideas to survive.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative and hypothetical. This material is intended for wholesale and professional investors.