Direction and Size

Why Conviction Comes in Degrees, and Portfolios Should Too

By the team at Banyantree Investment Group

Precision is a temperament: small adjustments, repeatable methods, and the refusal to guess when the margin for error is real. Beam compass and clamps. Central Intelligence Agency image archive. Cropped, redrawn, and colour-treated.

───

In the autumn of 1981, Ray Dalio was thirty-two years old and certain. Not cautiously certain, not hedgedly certain — certain in the way that allows a person to testify before the United States Congress and hear themselves speak without any trace of doubt. His research had led him to a conclusion that felt as close to arithmetic as analysis gets: the Federal Reserve had engineered a period of tight money, the world’s borrowing nations had accumulated debts they could not repay, and the only two responses available, default or inflation, would both be devastating. A depression was coming. He wrote about it in newspaper columns. He appeared on television to say so. He told Congress.

In August 1982, Mexico defaulted on its sovereign debt. The cascade he had predicted had begun. He was, by any reasonable measure, right.

And then Paul Volcker lowered interest rates and opened the liquidity taps, and the market did something Dalio had rated as improbable: it turned. The S&P 500 began a rally that would compound for nearly two decades. The greatest non-inflationary bull market in American history started almost exactly where Dalio had announced it would end.

He lost almost everything. He dismissed all of his employees until Bridgewater Associates consisted of one person: Dalio. He borrowed four thousand dollars from his father to cover his family’s bills. The experience, he would later write, was like being hit in the head with a baseball bat.

What had failed was not the underlying analysis. The debt was real. The default was real. His reading of the structural problem was, by most accounts, largely correct. What failed was the portfolio’s dependence on a thesis that needed to be right not just directionally, but in every important detail, including the policy response that Dalio had examined and dismissed. He had made a single, decisive mistake: he had confused the quality of his analysis with the completeness of his knowledge.

───

There is a question that gets asked in investment committee rooms so often, and in so many variations, that it has become a kind of institutional reflex. It goes like this: are we bullish or bearish? Risk on or risk off? Constructive or cautious? The question is not unreasonable. Portfolios must be positioned somehow, and a direction, towards risk or away from it, seems like a logical place to start.

The trouble is that this question contains a hidden second question, and the hidden question is the one that actually determines outcomes. Not: in which direction should we lean? But: how much should that lean weigh?

Direction and size are two separate decisions. Most of the error in professional investing lives in treating them as one.

The Sequoia Fund made this error in the other direction. Founded in 1970 by Bill Ruane, with Warren Buffett’s explicit blessing when he closed the Buffett Partnership and directed his departing partners towards Ruane’s care, Sequoia had spent forty-five years building one of the most admired records on Wall Street. Over that period it earned an annualised return of 14.65 per cent, outperforming the S&P 500 in 332 of 333 rolling ten-year windows. Its method was deliberate, long-horizon, concentrated. By mid-2015, Valeant Pharmaceuticals had grown to represent 32 per cent of the fund’s assets. Not through carelessness. Not through leverage. Through conviction: a thesis that was coherent, a stock that had been rising for years, and a management team that had not yet been caught.

When Valeant eventually imploded under the weight of its drug pricing practices, a pharmacy subsidiary scandal, and the regulatory attention that followed, it lost 93 per cent of its value from peak to trough. Sequoia fell 34 per cent over the same period, lagging the S&P 500 by 31 percentage points. Robert Goldfarb, CEO and co-manager for forty-five years, resigned. The fund was sued by its own shareholders. “That’s where we got in trouble,” co-manager David Poppe said afterward. “Where Bob said, ‘I’m right and you guys are wrong.’”

The direction was not obviously wrong. The sizing was fatal.

Dalio had bet everything on a macro scenario. Goldfarb had bet everything on a single stock. The mechanisms were different. The root error was identical: each had allowed conviction to collapse into certainty, and certainty into size.

───

There is a useful distinction buried inside the Dalio story, one he spent the next several decades building an investment organisation around.

Some of what goes into a thesis is knowable, not with perfect precision, but with genuine analytical grounding. Balance sheet strength is observable. Cash generation is measurable. Competitive position can be examined, stress-tested, and updated as evidence arrives. Valuation can be assessed against a range of outcomes. Management quality can be studied. These inputs can be evaluated. They provide a foundation.

What cannot be known, in any serious sense, is the set of contingent facts that surround them: the timing of when a thesis resolves, the policy decisions of central banks operating under pressure, the regulatory attention that will eventually fall on a particular business model, the competitor response that is still being planned in another building. Dalio knew about the debt. He did not know how Volcker would respond to it. Sequoia understood Valeant’s model. They did not know about the pharmacy subsidiary, or the precise combination of congressional scrutiny and accounting restatements that would destroy investor confidence in a single season.

This distinction, between what a thesis can know and what it cannot, is the engine inside a non-binary portfolio.

The knowable supports a direction. It gives grounds for wanting exposure, for finding a thesis worth holding. The unknowable constrains the size. It sets a ceiling on how much of the portfolio a single set of assumptions is allowed to control. Because the unknowable is not a temporary condition to be resolved with more research. It is structural. It is the gap between analysis and outcome that exists in every investment, at every conviction level, regardless of how thoroughly the knowable has been examined. Acknowledging it is not timidity. It is precision.

Plan for what we know. Plan, also, for what we cannot.

───

The practical question is how to convert that distinction into portfolio construction without turning every sizing decision into an abstract epistemology exercise: treat conviction as a spectrum, and let position size follow it.

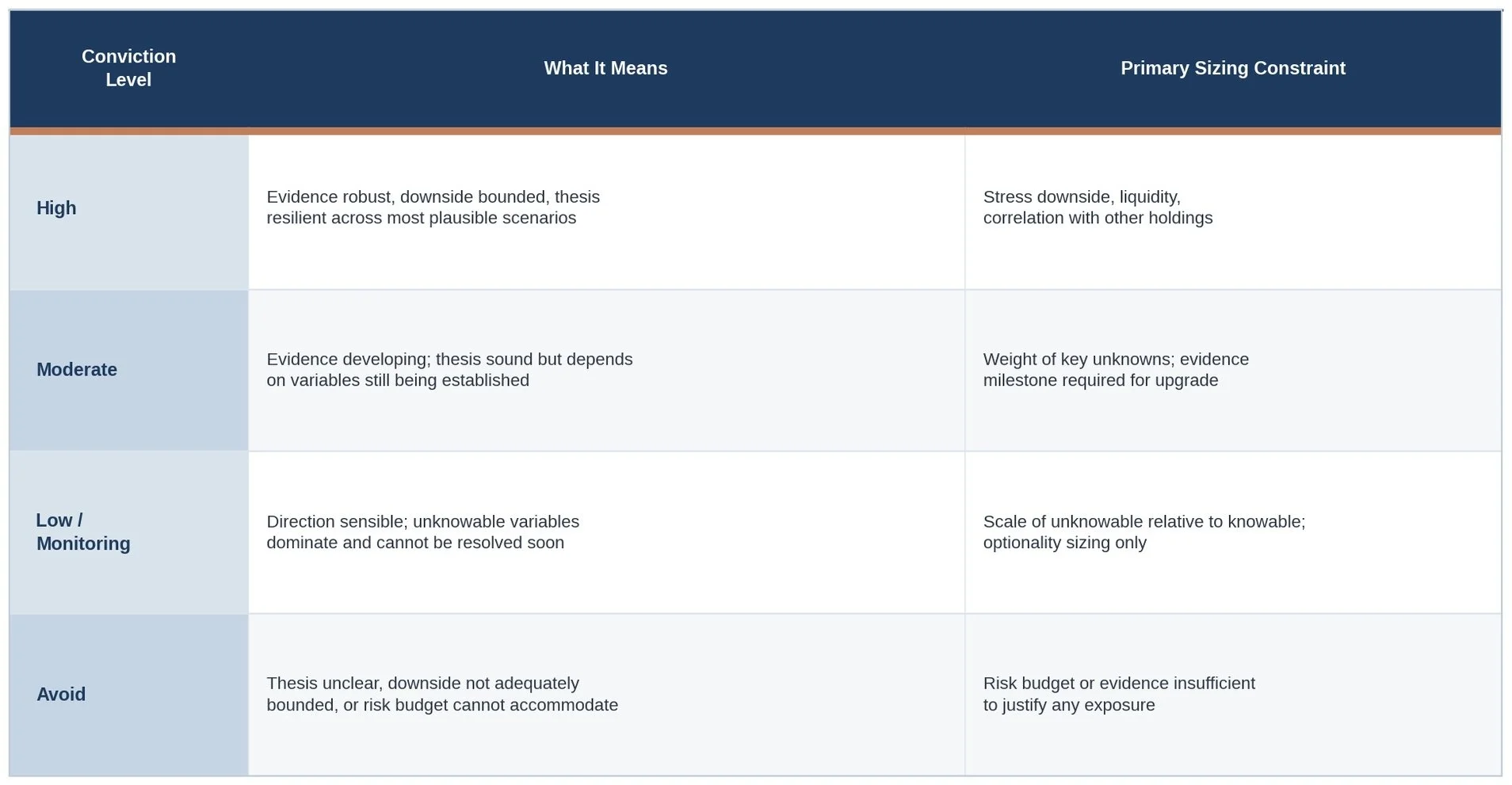

At the high end sits a position where the evidence is clear, the downside is bounded, and the thesis remains intact under most of the scenarios that matter. The unknowable elements are present, as they always are, but they do not dominate the range of plausible outcomes. This earns a larger weight: not because nothing can go wrong, but because the portfolio is not being asked to assume nothing will. At the moderate level, the evidence is developing, the thesis is sound but depends on something still unresolved, or the downside requires a meaningful correction to one or two assumptions. This earns a smaller weight. At the low end, the direction may still be sensible, but the material unknowns are significant enough that the position functions primarily as optionality: exposure to an opportunity that might deserve more weight when the picture clarifies. And then there are positions to avoid altogether, not because the idea lacks merit, but because the gap between what is knowable and what is required cannot be sized safely within any sensible loss budget.

Conviction sets size. Uncertainty sets diversification.

The corollary deserves equal emphasis. Diversification, spread across positions where conviction has not been earned, is not a slogan or a comfort blanket. It is an acknowledgement of what the portfolio does not yet know, deployed deliberately rather than sprayed indiscriminately. A portfolio full of positions owned at equal weight regardless of evidence quality is not diversified. It is indifferent. A portfolio where the largest positions carry the most robust evidence, and the smaller positions carry the most uncertainty, is doing something more considered: it is allowing the knowable to set the hierarchy.

Concentration is not the opposite of this discipline. It is the product of it. Concentration is earned; diversification is used where conviction is not.

The Conviction Spectrum

Conviction is not a personality trait. It is a funding decision under uncertainty. The point of the spectrum is to make that decision explicit, and to stop pretending that “maybe” and “yes” should be sized the same. Illustrative and hypothetical.

The table that follows defines what each level means in practice and what governs the sizing decision within it.

───

Exhibit 1. Conviction Spectrum — Definitions and Sizing Constraints

Words like “high conviction” are cheap until they have constraints. What matters is not the label, but what caps the size: downside, liquidity, correlation, or simply how much you still don’t know. Illustrative and hypothetical.

───

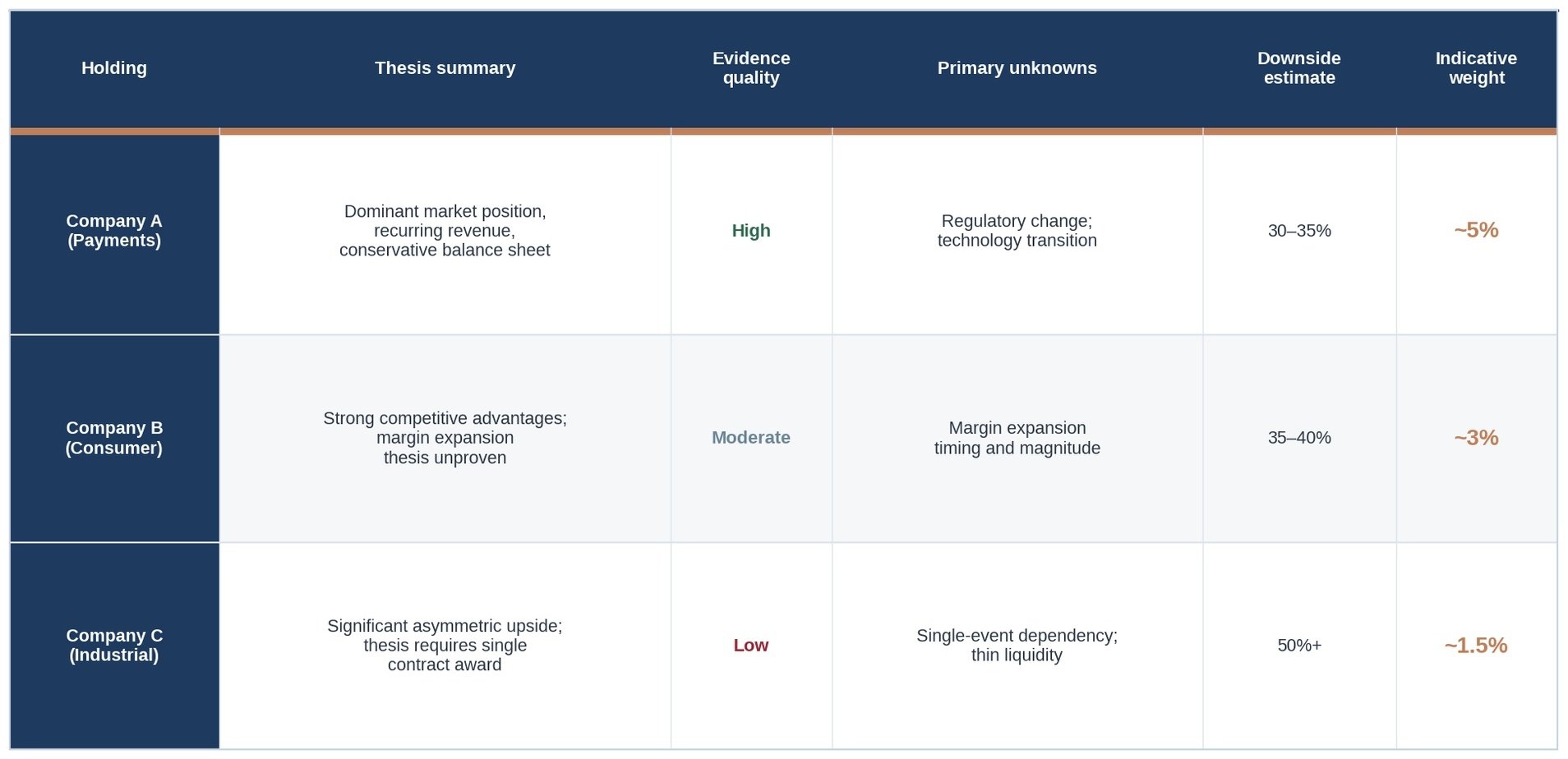

A portfolio team is evaluating three positions. The first is a payments infrastructure business with dominant market position, recurring revenue, and a conservative balance sheet. The valuation is full but defensible across a reasonable range of growth assumptions. The thesis is robust across most scenarios; the downside in a stress case is meaningful but bounded. The unknowns are real, regulatory change and a technology transition among them, but none dominates the range of plausible outcomes. Conviction is high. The position earns a weight at the upper end of the sizing bands.

The second is a consumer business with genuine competitive advantages but a thesis that depends partly on margin expansion that has not yet materialised. The direction is clear; the evidence is developing. One or two reporting periods would sharpen the picture considerably. The unknowns are not disqualifying, but they are material. Conviction is moderate. The position earns a smaller weight: exposure to a thesis worth holding, sized to reflect that something important is still being established.

The third is an early-stage industrial business with significant asymmetric upside and thin liquidity. The thesis requires a single event, a contract award that would confirm a market position. The direction may be right; the entire outcome depends on one thing that cannot be known in advance. Conviction is low, not because the idea lacks merit, but because the unknowable is the thesis. The position earns a minimal weight, functioning as optionality rather than a core contributor.

───

Exhibit 2. Three Holdings, Three Conviction Levels, Three Weights

Sizing is how research becomes behaviour. The same optimism can produce radically different weights once you force yourself to write down the unknowns and price the downside. Illustrative and hypothetical.

───

The portfolio that results from this process is not cautious. It holds a meaningful position in the first business precisely because the evidence warrants it. It is not indifferent. The second and third businesses are held at weights that reflect what is actually known about them, rather than what the team hopes will eventually become known. The aggregate expresses genuine views, without requiring those views to be entirely right.

───

What would change this view?

One genuine challenge: if the gap between knowable and unknowable could be meaningfully compressed, if evidence quality for investment theses became reliably more complete, more quickly, and at lower cost, then the argument for graduated sizing would weaken at the margin. Better information reduces the penalty for concentration. But this compression has not occurred in the ways that matter most. The things that tend to destroy portfolios, policy responses, competitive reactions, the precise timing of when a thesis resolves, remain stubbornly resistant to analysis. More data has not made them more predictable.

A second challenge: some mandates are structurally constrained in ways that make fine graduation impractical. A fund with narrow weight limits or many required positions cannot easily express a four-tier conviction spectrum. Where the implementation levers are limited, the principle must be adapted rather than abandoned. The adjustment is not to ignore conviction quality but to express it through the tools available: higher or lower weights within narrower bands, more or less liquidity held alongside, more or fewer positions diversifying a thesis whose central unknowns remain large.

Neither condition, in its current form, overturns the underlying logic. Both deserve acknowledgement.

───

After 1982, Dalio rebuilt Bridgewater around a principle he later articulated as fifteen good uncorrelated return streams, a portfolio designed to hold up across a wide range of economic environments, including environments he had not predicted. He did not stop having views. He did not become uncertain about everything. He stopped needing his views to be entirely right in order for the portfolio to survive.

That is what a non-binary portfolio is. It is not a portfolio without convictions. It is a portfolio whose convictions have been sized to reflect what those convictions actually are — a reading of the knowable, accompanied by an honest accounting of what cannot be known. It can hold a large position in something it understands well, a smaller position in something it understands partially, and a minimal position in something whose outcome depends on a variable that analysis cannot resolve. It can hold all three simultaneously, without contradiction, because the sizing is doing the work that certainty is not entitled to do.

Direction is one decision. Size is another.

A portfolio that requires its convictions to be right is not a portfolio. It is a bet.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative and hypothetical. This material is intended for wholesale and professional investors.