Insights from Our Recent Travels: Six Investor Signals from Asia and the Gulf

Zach Riaz speaking during a panel discussion at AIM Summit Dubai (22–23 October 2025).

We have just returned from meetings and conferences in Hong Kong, South Korea, and the UAE (Dubai). The purpose of the trip was simple: speak to fund managers, family offices, and companies that are deploying capital right now, and understand what is genuinely on their minds. Because the conversations spanned regions, and different types of investors, we were able to see the common threads quite clearly. Six themes stood out.

1. Investors are cautious, although they are not de-risking

Almost every investor we met described the current market environment as uncomfortable. Several said they struggled to reconcile the strength of the equity rally with valuations in parts of the market, particularly where earnings visibility is weak. Yet not one of them said they were on the sidelines, or holding excessive cash. In practice, portfolios are still fully invested.

We read this as a classic “reluctant long” position. Investors can see where the pockets of exuberance are, however, they do not want to miss performance while liquidity is still supportive, and policy may yet provide a further cushion.

2. The bigger the economic/market impact, the larger the policy response

You may have heard of the saying, “Don’t fight the Fed.” However, what you should also be paying attention to is, “Don’t fight the Treasury.” Many are suggesting that the current US Treasury Secretary, Scott Bessent, will likely go down as one of the most interventionist Treasury Secretaries in history.

That is, his department has shown a strong willingness to support the economy, and it has various tools to impact asset prices. One key focus for Mr Bessent is to keep the US 10-year Treasury yields lower (that is, keep the US Government’s borrowing costs low), and he can impact this through regulation, issuance, and tax policy.

The takeaway expressed to us was simple: the bigger the potential shock, the bigger the likely policy response. That is one reason many investors are reluctant to de-risk too early.

3. Constructive on the United States, although succession is a live risk

A good number of investors were positively disposed towards the US outlook. They cited:

— the pro-growth tilt of President Trump’s administration,

— the continued focus on deregulation,

— the technology and AI build-out, and

— a Federal Reserve that is expected to ease further over the next 12 months.

This view is helped by the condition of the US household sector. Debt-service payments as a share of disposable personal income remain below pre-COVID levels, which means the consumer still has room to support growth.

Figure 1: US household debt servicing remains below pre-COVID levels

Household debt-service payments as a percentage of disposable personal income (US). Shaded areas indicate US recessions. Source: Board of Governors of the Federal Reserve System (US) via FRED®; analysis: Banyantree.

What could upset this otherwise positive US picture is politics. Several investors raised the obvious point that President Trump is 79, and that an abrupt transition to Vice President JD Vance would likely mean a more isolationist and more protectionist policy stance than the President has pursued. It was not described to us as a base case, although it was consistently described as the risk that markets would find most disruptive.

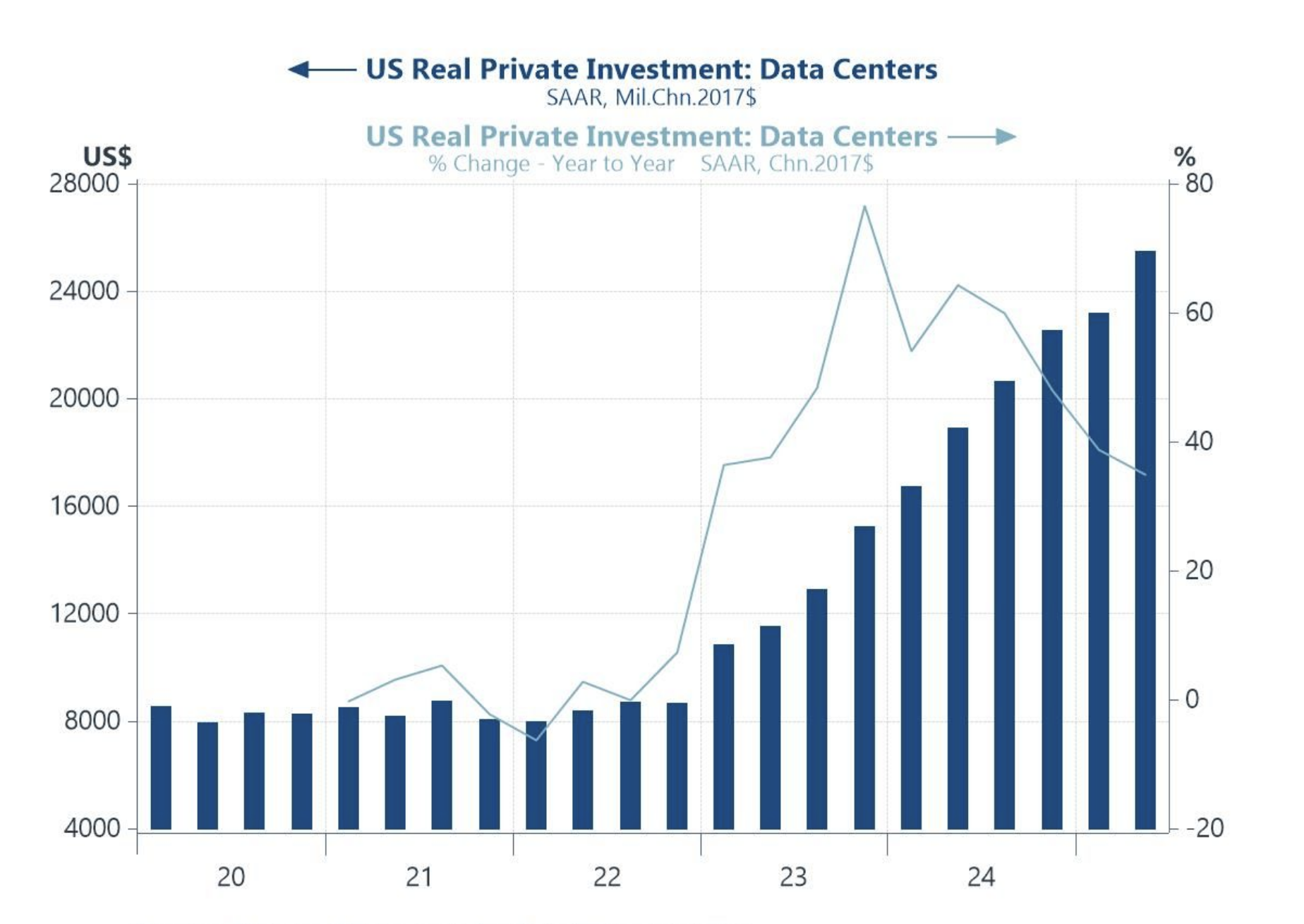

4. The AI build cycle is still running, led by the United States

There was broad agreement that the AI capital-expenditure cycle has more room to go. What was equally clear was that the United States is leading this phase, while Europe and parts of Asia are still catching up. The data on US real private investment in data centres show a very strong lift.

Figure 2: US data-centre investment has stepped up as the AI build-out continues

US real private investment in data centres (SAAR, US$m, chained 2017 dollars) and year-on-year % change. Source: Bureau of Economic Analysis via Haver Analytics; analysis: Banyantree.

5. Private credit was a big talking point

Some of the family offices we spoke with are increasing their exposure to private credit. The funding source for this exposure will be reducing allocation to private equity.

In their view, private credit is offering more alpha opportunities compared to the listed market, which is competitive. Nonetheless, the recent media coverage of a potential emerging default cycle in the private-credit sector does have some investors concerned, but they will look at this as a buying opportunity (they prefer asset-backed private credit). Long-term, they expect the private-credit market to grow to a US$5 trillion industry.

Figure 3: US banks’ lending to private credit is now a major balance-sheet exposure

Amount in loans to private credit firms by major US banks (US$bn). Source: Bloomberg; compiled by Bluekurtic Market Insights; analysis: Banyantree.

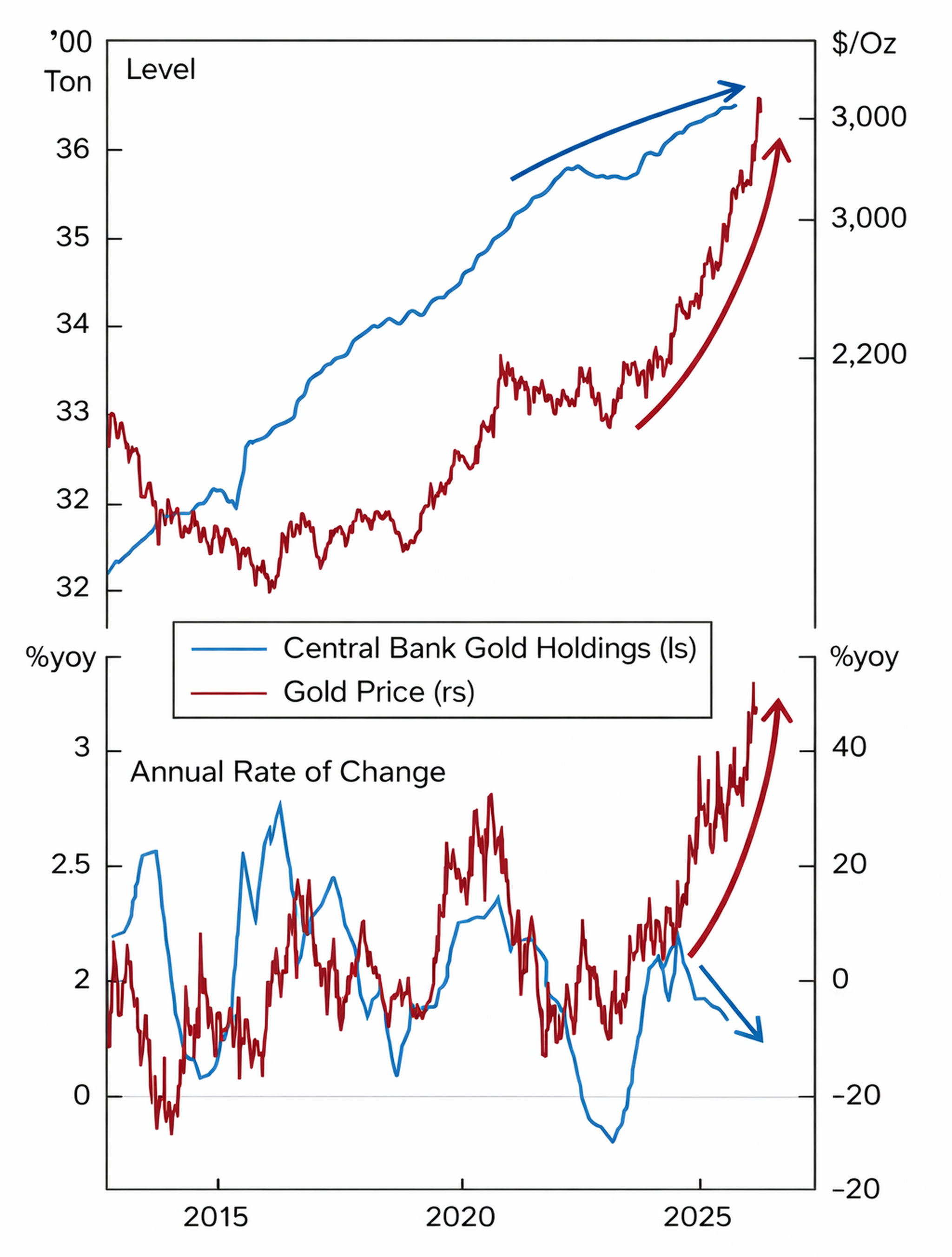

6. Gold: still a supportive medium-term case, although profit-taking is prudent

“Gold is in a bubble” came up repeatedly. The price did correct more than 8 per cent recently. We had already reminded clients to take some profits. The medium-term case has not changed, however, central-bank buying has moderated, which means investors are now doing more of the work.

Figure 4: Gold prices are doing more of the work as central-bank buying cools

Central bank gold holdings (tonnes, lhs) and gold price (US$/oz, rhs), plus annual rate of change (% y/y). Source: Alpine Macro / World Gold Council; analysis: Banyantree.