Looking back at our 2025 non-consensus calls

Five big calls we made in January and how they played out in markets and portfolios.

In January 2025 we set out five “controversial, non-consensus” calls for the year ahead.

With most of the year now behind us and our 2026 outlook in the works, it’s a good time to look back at those calls, what actually happened, and what mattered for portfolios including where we were early, where we were wrong, and what we learnt along the way.

This isn’t about keeping score for the sake of it. The point is to show our process in public: we form a view, write it down, size the risk, and then compare outcomes to the thesis.

1. “The bull market will continue: expect double-digit returns over the next two years.”

Call: Global equities would remain in a bull market, delivering double-digit returns over 2025-26.

Outcome so far: Correct (so far). Year-to-date, major equity indices have delivered very strong returns in USD terms:

— MSCI World Index: +23.4%

— S&P 500: +20.1%

— NASDAQ Composite: +25.2%

— FTSE 100: +22.9% (GBP)

— German DAX: +21.8% (EUR)

Exhibit 1: Major equity indices delivered strong YTD returns in 2025.

The path hasn’t been smooth. We saw a meaningful sell-off in April, driven by worries about policy, inflation and earnings.

We did use that drawdown as an opportunity to add risk selectively, consistent with the original call: when the underlying earnings and policy picture still support the cycle, broad sell-offs are often better used to upgrade portfolios than to de-risk them.

What mattered for portfolios

— Staying invested in quality names and not treating every wobble as the end of the cycle.

— Using pre-set ranges and signposts to distinguish a normal shake-out from a genuine regime change.

We still expect the next two-year period to be driven more by earnings and valuation discipline than by multiple expansion alone. The easy part of the bull market is behind us.

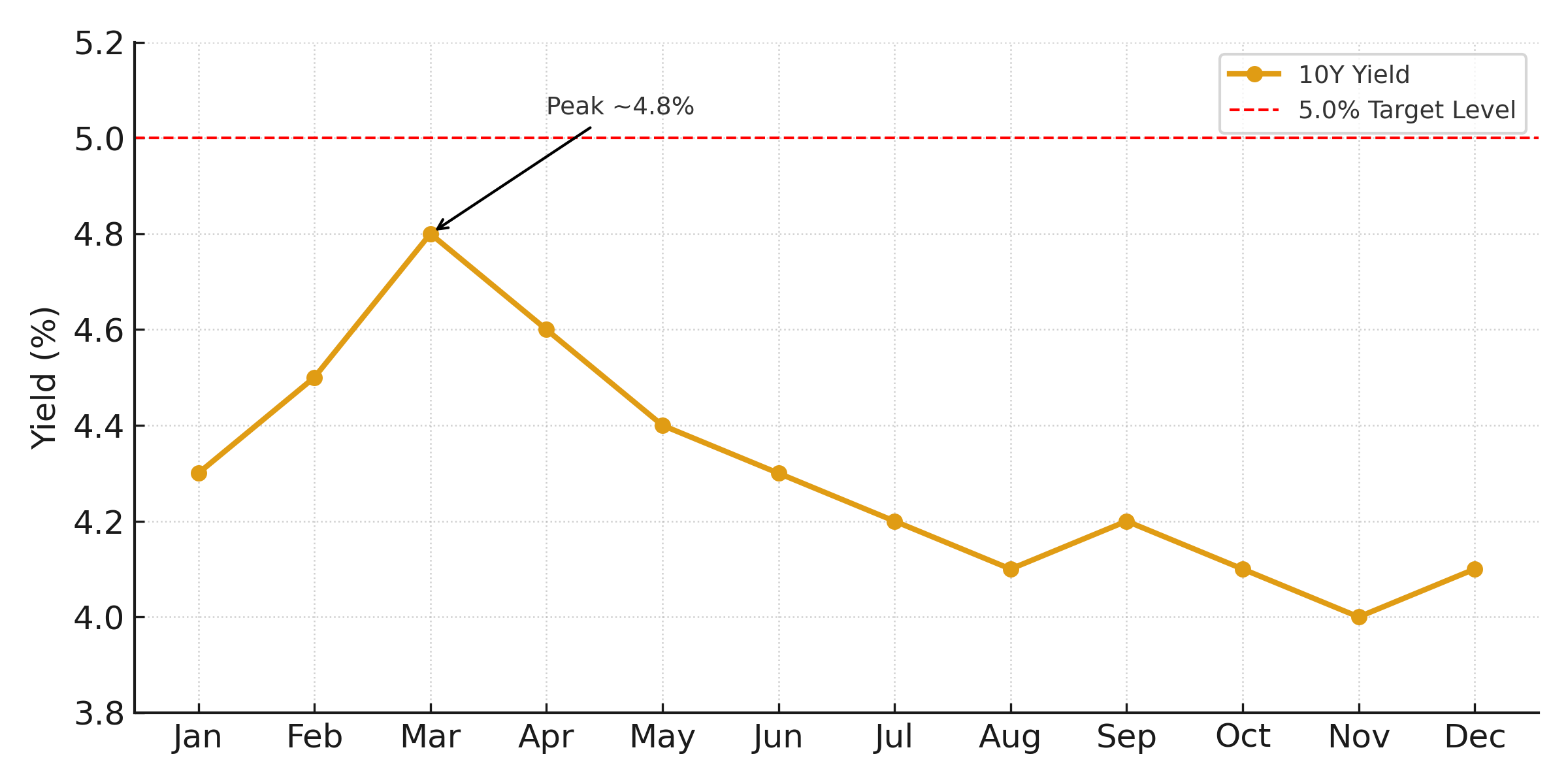

2. “The U.S. 10-year Treasury yield will spike well above 5.0%.”

Call: The US 10-year yield would break decisively above 5.0%, reflecting sticky inflation, large fiscal deficits and term-premium normalisation.

Outcome so far: Wrong.

Exhibit 2: The U.S. 10-year Treasury yield peaked around 4.8% and never breached 5%.

The 10-year did push up towards 4.8% early in calendar 2025, but since then has traded in a relatively tight range in the low 4s, as markets became more comfortable with the disinflation path and the pace of policy moves.

The fundamental forces behind the call, heavy Treasury supply, higher equilibrium real rates, and geopolitical risk premia, remain in place. But the combination of softer data, credible central bank communication and strong demand for yield has, so far, capped the move.

What mattered for portfolios

Even though the exact yield level didn’t materialise, the preparation for that scenario still influenced how we positioned:

— We remained cautious on long-duration government bonds at unattractive yields.

— We continued to prefer shorter-duration exposure and high-quality credit where compensation for risk was clearer.

This is a good example of why we frame views as ranges and scenarios, not precise price targets. The direction of travel can still be useful, even if the destination is different.

3. “Gold’s spot price will hit US$3,500.”

Call: Gold would move significantly higher, breaching US$3,500 an ounce as investors looked for insurance against policy and geopolitical risk.

Outcome so far: Correct and then some.

Exhibit 3: Gold spot price moved well beyond our original $3,500 target, finishing 2025 near $4,191.

Gold started the year around US$2,600 and has since climbed to roughly US$4,191 per ounce. That’s well beyond our original target.

Several forces have contributed:

— Concerns about fiscal sustainability and debt dynamics.

— Persistent geopolitical tension, including in Eastern Europe and the Indo-Pacific.

— Central bank buying and a broader search for assets perceived as stores of value.

What mattered for portfolios

We viewed gold less as a directional “trade” and more as portfolio insurance:

— A modest allocation can help when real yields, currencies or risk assets are behaving unpredictably.

— The position size is anchored to its role as a hedge, not a bet that must be “right” every year.

The lesson here is that when you own an asset as insurance, you size it so that it still makes sense even if the upside overshoots your base case.

4. “Donald Trump and Xi Jinping will call a truce on the U.S.–China trade war.”

Call: Trade tensions between the US and China would ease, with a de-facto truce rather than escalation.

Outcome so far: Broadly correct, with nuance.

This was less about a grand, formal peace deal and more about the tone and direction of policy. Through 2025, we’ve seen:

— A softer rhetorical stance at key moments.

— A noticeable stepping back of the most aggressive “China hawk” positions in Washington.

— Some willingness, on both sides, to stabilise economic ties where interests align.

To us, it has been “patently clear” that outright escalation has been deprioritised, even if the relationship remains strategically competitive.

What mattered for portfolios

— The reduced probability of an acute trade shock has been supportive for risk assets, particularly in sectors exposed to global supply chains.

— At the same time, we remain very selective on China-related exposures and assume that geopolitical risk premia are structurally higher than a decade ago.

In other words, this is a truce, not a reversion to the pre-trade-war status quo.

5. “Natural gas starts a bull run.”

Call: Natural gas would break out of its doldrums and begin a sustained bull move.

Outcome so far: Correct.

Exhibit 4: Henry Hub natural gas price rose sharply through 2025, reflecting tighter supply and strong LNG demand.

Henry Hub natural gas prices are up around +47.7% year-to-date to roughly US$5.02 per mmBtu. The drivers have been:

— Extreme and volatile weather patterns.

— Strong global demand for liquefied natural gas (LNG).

— Ongoing supply and infrastructure bottlenecks in key regions.

What mattered for portfolios

— Understanding the linkage between gas prices, inflation expectations, and sectors such as utilities, chemicals and parts of industrials.

— Treating energy exposures as risk positions with clear exit rules, not open-ended “macro themes”.

This is an area where we expect volatility to remain elevated. The focus is on disciplined sizing and clarity about what would change our view.

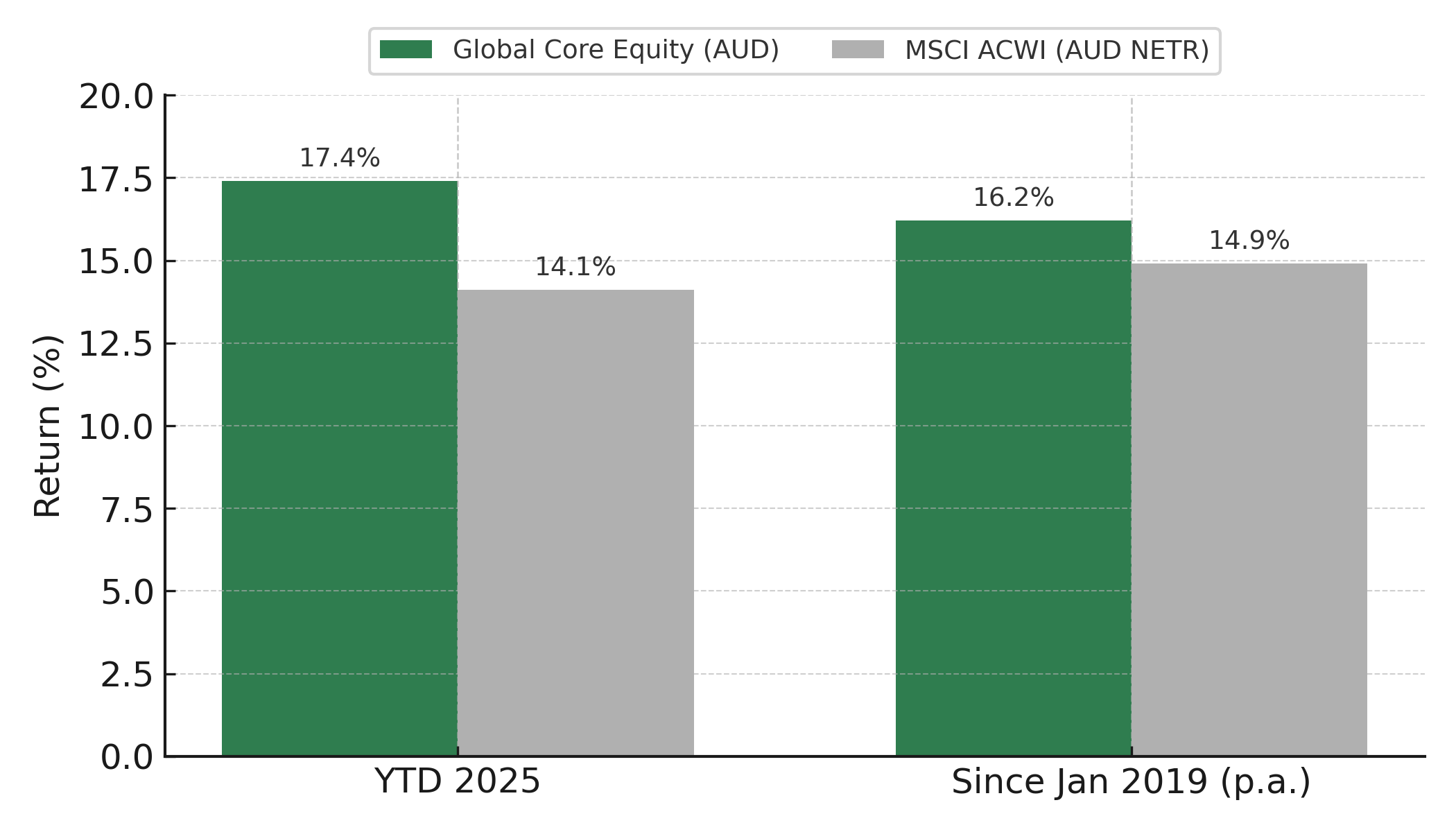

Portfolio results: Global Core Equity and a stock pick that ran

Against this backdrop, our Banyantree Global Core Equity Strategy (AUD) has delivered:

— +17.4% year-to-date, versus +14.1% for the MSCI ACWI AUD NETR.

— Since inception in January 2019: +16.2% p.a., versus +14.9% p.a. for the benchmark.

Exhibit 5: Global Core Equity Strategy performance versus MSCI ACWI AUD NETR.

Past performance is not a reliable indicator of future performance. Returns will differ for individual investors depending on timing, fees and implementation.

Our key Australian stock pick for 2025 was Life 360 Inc (ASX: 360). It’s up roughly +75% year-to-date, and we continue to hold the position in our portfolios.

Again, the point is less about a single name and more about the process: clear thesis, measured sizing, and pre-defined signposts for when the story changes.

What this review means for 2026

Looking back at these non-consensus calls, three themes stand out as we shape our 2026 outlook:

Writing it down matters.

Having our views and ranges documented makes it easier to judge where we were right for the right reasons, right for the wrong reasons, or simply early.Risk first, returns second.

Even when a call is “wrong” in a narrow sense (like the 10-year yield not breaking above 5%), the risk work behind it can still improve portfolio construction, for example, by avoiding uncompensated duration risk.Non-consensus doesn’t mean reckless.

Being willing to deviate from consensus is important, but it has to sit inside a disciplined framework of mandates, size bands, liquidity floors and exit rules.

We’ll share more detail on our 2026 views in due course. In the meantime, if you’re an adviser or wholesale investor and would like to dig into any of these themes, we’re always happy to have a conversation.

General advice only. This material has been prepared for wholesale and professional investors and does not take into account your objectives, financial situation or needs. Past performance is not a reliable indicator of future performance.