Size Before Return

Downside sets position size. Expected return sets the order of priority. The portfolio that reverses that sequence does not discover the error until the market tests it.

15 min read | By the team at Banyantree Investment Group

Before a risk could be assumed in this room, its maximum had to be written down: the slip, the line, and the number its author was prepared to lose. Lloyd's of London underwriting room. Artist's reconstruction. Cropped, redrawn, and colour-treated.

───

At seven o’clock on the evening of Thursday, 25 March 2021, Bill Hwang picked up the phone and did something he had spent a career avoiding. He asked for help.

Hwang was not a man who negotiated from weakness. A protégé of Julian Robertson at Tiger Management, he had built Archegos Capital Management into a family office controlling positions worth more than thirty billion dollars, a figure that, had it been widely known, would have placed him among the largest holders of equities on earth. He had done it quietly, using total return swaps that allowed him to command enormous economic exposure to stocks without technically owning them and without triggering the disclosure rules that applied to conventional shareholders. The method was legal. The scale was breathtaking. In several companies, Archegos controlled more than half the tradeable float, and the market had no idea.

The positions were not exotic. ViacomCBS. Discovery. Baidu. GSX Techedu. Real businesses with identifiable models and, in several cases, genuinely defensible investment theses. Hwang was not a gambler reaching for lottery tickets. He was a concentrated investor who had been right, repeatedly, for years, and who had used that track record to extract more and more leverage from the prime brokers competing for his business.

But earlier that week, ViacomCBS had announced a secondary stock offering. The share price dropped. Then it dropped further. The banks on the other end of Hwang’s swaps, Goldman Sachs, Morgan Stanley, Credit Suisse, Nomura, and others, were doing arithmetic of their own. They wanted more collateral. Hwang wanted time. The Thursday evening call was his attempt to hold the coalition together: to persuade the banks to act in concert rather than in self-interest, to give the positions room to recover before anyone rushed for the exit.

Think about what he was asking. He needed a handful of competing investment banks, each with its own risk committee and its own profit-and-loss statement, to trust one another enough to sit still while billions of dollars in collateral requirements went unmet. It was the kind of coordination that works only when everyone believes the alternative is worse. By Thursday night, not everyone did.

The call ended without agreement. By Friday morning, Goldman Sachs had begun liquidating. Morgan Stanley followed. Block trades totalling roughly fifteen billion dollars hit the market before most investors had finished their coffee. The stocks cratered, which triggered further margin calls at the slower banks, which triggered further selling. By Monday, Archegos was gone: not wounded, not restructured, but erased. Hwang’s personal fortune, estimated days earlier at twenty billion dollars, had effectively ceased to exist. Credit Suisse, which had hesitated while its American counterparts moved, eventually wrote off 5.5 billion dollars. The loss contributed to a crisis that would end with the bank’s forced sale to UBS two years later.

The post-mortems focused on leverage and disclosure, and those were real issues. But the deeper failure was older and more common than any regulatory loophole. It was a failure of sizing. Hwang had built positions so large relative to his capital that the thesis didn’t need to be wrong. It merely needed to be late.

He had built a portfolio that could not survive being wrong.

───

The arithmetic inside that collapse applies, with different intensity, to every portfolio that has ever been built. Hwang’s concentrated positions, levered five to one, didn’t just hurt five times as much when they fell. They could extinguish the entire stake and leave him owing money on the remainder. But the underlying maths belongs to everyone.

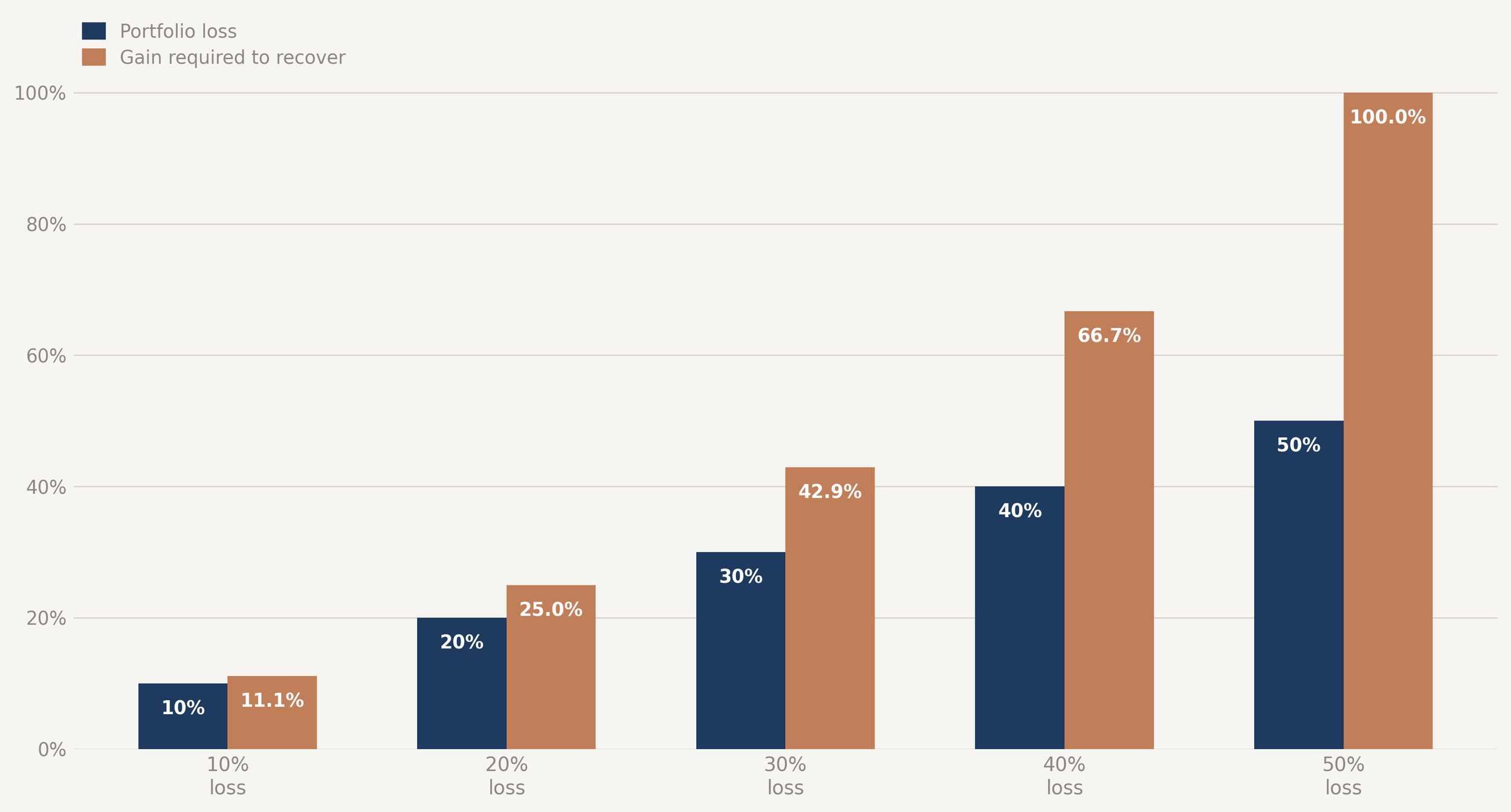

A portfolio that falls ten per cent needs an eleven per cent gain to recover. At twenty per cent down, you need twenty-five per cent back. At fifty per cent, a level the S&P 500 has approached or breached several times since 1950, you need one hundred per cent just to return to where you started.

Exhibit 1 : The Asymmetry of Drawdown Recovery

Recovery gains required after losses of increasing size, showing the non-linear widening of the gap between loss and recovery. Hypothetical. Illustrative only. Not personal advice.

These are not just numbers on a quarterly statement. A drawdown alters the conditions under which every subsequent decision gets made. Committees shorten their horizons. Mandates get rewritten. Clients who swore they were long-term investors discover, under the specific pressure of watching real money disappear, that their actual tolerance for pain is considerably lower than the version they described in calmer rooms in easier times. And selling, which looked like one option among many when markets were orderly, reveals itself as the only tool left: exercised at prices nobody would have accepted a month earlier, into liquidity that has evaporated precisely when it was needed most.

This is how most portfolios fail. Not because the underlying ideas were foolish, but because the ideas were sized as if drawdowns were optional and liquidity was guaranteed.

───

The industry builds portfolios the other way around. You identify an investment with an attractive expected return. You take a meaningful position, large enough to make it matter. Then you check the risk metrics afterward, the way a driver checks the mirrors after merging. It sounds sensible because, most of the time, it is. The trouble is that most of the time is not the period that determines outcomes.

In any investment committee, you will hear the same argument, phrased with minor variations, about different companies, from different analysts, in different years: this position is different. The thesis is strong. The management team is excellent. The valuation is undemanding. All of which may be true. None of which tells you how the position will behave when the market stops caring about the thesis. The tendency to forecast based on the specifics of the case in front of you, while ignoring the base rate of how similar cases have turned out, is one of the most durable errors in human reasoning. It survives intelligence, experience, and credentials. It thrives in committees because committees reward confidence in the specific and punish attention to the general.

The base rate is blunt. Drawdowns happen. Correlations rise in stress. Liquidity disappears when you need it most. Return-first sizing plans for the specific case. Risk-first sizing plans for the base rate.

───

A risk-first portfolio begins with a question that most portfolios never explicitly answer: how much can this portfolio lose, under realistic stress, without triggering forced selling, a mandate breach, or strategy abandonment?

Call it a loss budget. What you are really doing is converting tolerance for pain from a vague sentiment, interpreted differently by different members of the same committee, into a design constraint that can be measured and held steady across market cycles. Written down as a number and stress-tested against history, it becomes architecture.

Once you have a loss budget, position sizing becomes arithmetic rather than enthusiasm. The rule is plain enough to write on an index card:

Downside sets size; expected return sets order.

For any position, you define a plausible stress scenario: not the worst case imaginable, but a realistic adverse outcome you can articulate in plain language. What happens if the thesis is wrong in a normal way? What happens if it is wrong in a bad way, or the market de-rates the entire sector, or both? Then you ask how much of this loss the portfolio can absorb without triggering the kind of decision-forcing event, a margin call, a mandate breach, a panicked board meeting, that turns temporary pain into permanent impairment.

The maximum position size flows directly from that constraint. If the loss budget allows a single position to cost the portfolio no more than two per cent in a stress scenario, and the stress downside for the position is forty per cent, the arithmetic gives a starting size of five per cent. Not because five per cent feels right, but because five per cent is the answer to a question that was actually asked.

Then you adjust for the things that show up late in cycles and early in crises: liquidity that may not exist when you need it, and correlation with other positions that may spike precisely when you hoped they would diversify.

Only after size is set does expected return enter the conversation. Not to determine how much you own, but to determine priority among ideas competing for limited risk budget. The sequence matters.

───

A portfolio team is evaluating a European payments company: a genuine compounder with dominant market share, subscription-like revenue, and a management team that has executed well for a decade. The stock trades at thirty-eight times earnings, expensive by historical standards but defensible given the growth profile. The bull case offers fifteen per cent annualised returns over five years. It is exactly the kind of position that return-first thinking wants to make large, because the business is so obviously good.

The stress case is different. Multiple compression to twenty-two times earnings, plus a modest earnings cut in a recession, implies a forty per cent drawdown. The company would still be a fine business at the bottom. The question is whether the portfolio can still be a fine portfolio at the bottom.

Return-first thinking asks: how much do we need to own to make this position matter? Risk-first thinking asks: how much can we own without this breaking the portfolio?

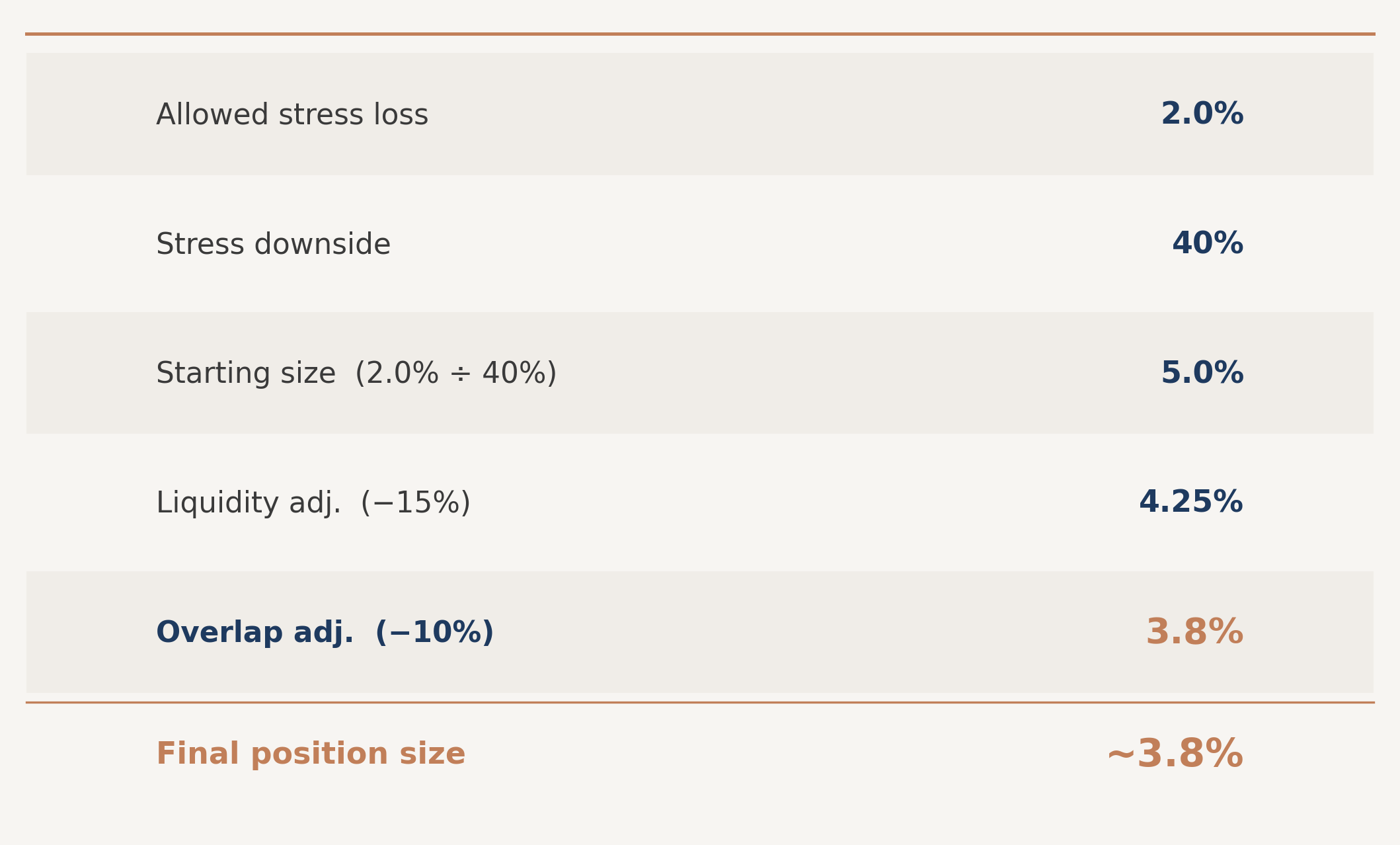

Assume a loss budget of twelve per cent for the total portfolio, and a rule that no single holding should contribute more than two per cent of portfolio-level stress loss.

The arithmetic establishes a starting point of five per cent: the two per cent single-name loss limit divided by the forty per cent stress scenario. Two conditions then push it lower, both visible before the position is opened. This is a crowded name, heavily owned by comparable funds; in a broad de-rating, the portfolio would not be the only seller, and that exit problem has a cost. The position also correlates closely with the quality-growth holdings already in the book: the same scenario that hits the payments company hits the rest of that sleeve simultaneously. The exhibit below runs the adjustments. The point is not the precise final figure. It is that the figure came from somewhere, that someone asked a question before they sized.

Exhibit 2 : Position Sizing — Worked Example

Starting size derived from a twelve per cent loss budget and a two per cent single-name limit applied to a forty per cent stress drawdown, reduced further for crowding and correlation. Hypothetical. Illustrative only. Not personal advice.

The return-first instinct protests. At eight per cent of the portfolio, this beautiful compounder would really move the needle. But at eight per cent, the same forty per cent stress scenario costs the portfolio 3.2 per cent from a single name, before accounting for the correlated holdings falling alongside it. String three or four such positions together and a portfolio of individually excellent ideas becomes collectively unsurvivable. That is how a portfolio becomes a collection of good theses that cannot survive contact with a bad market.

───

This is sometimes misread as an argument against conviction. It is not. It is an argument for earned concentration.

The distinction matters because conviction is one of the most abused words in professional investing. It gets used to describe a feeling: the warmth of a well-rehearsed thesis, the comfort of a management team that returns your calls, the private satisfaction of having been early. It should describe a position that has survived a genuine constraint. Concentration is earned only when three conditions hold: the downside is bounded in a way you can explain to someone who disagrees with you, the exit is feasible under stress, and the position does not simply duplicate risks the portfolio already carries. If those conditions are not met, concentration is not confidence. It is an accident waiting for a catalyst.

There is a tell that appears in portfolio reviews. When a position has done well, commentary focuses on the thesis: management execution, margin expansion, market share gains. Everyone takes credit for the return. When the same position is down thirty per cent, commentary shifts quietly from thesis to sizing: it’s only three per cent of the portfolio. The thesis was the reason for owning it. The size becomes the excuse for still owning it.

This sleight of hand is seductive because it works in both directions simultaneously. On the way up, a large position proves conviction. On the way down, a position that has become small through losses proves diversification. The narrative reshapes itself around the outcome, and nobody has to confront the possibility that the sizing was never the product of a deliberate decision at all: that it was simply whatever felt right when the trade was put on, later ratified by whichever direction the market happened to move.

The arithmetic makes the point more directly. A position sized to five per cent that subsequently falls forty per cent costs the portfolio two per cent. Uncomfortable, but survivable. The same position at twelve per cent costs nearly five per cent from a single name, before the correlated holdings fall alongside it. The question almost never gets asked before the fact. After the fact, it arrives in the wrong tense.

Risk-first sizing eliminates this by forcing the conversation to happen before the outcome is known. When the position falls, the committee is not improvising an explanation. It is reading from a document it wrote in a calmer room.

───

Risk-first portfolios will lag in strong, narrow bull markets. There is no version of this framework that avoids that cost, and a vague acknowledgement of the trade-off is not an acknowledgement at all.

When markets reward concentration, leverage, or crowding into the same handful of winners, and they do, reliably, for stretches that can last years, a portfolio sized to survive stress will not keep pace with portfolios sized to maximise exposure. In the years when everything goes right, the disciplined portfolio looks timid. The leveraged portfolio looks visionary. The manager who sized to risk will spend committee meetings explaining a process. The manager who sized to return will spend them accepting congratulations.

This is not an abstract cost. It is a felt one. It means watching a competitor who bought twice as much of the same stock report twice the return, knowing the thesis was equally understood and the same conclusion was reached, with the only difference being a willingness to bear a risk that was declined. It means sitting in review meetings where the question is not “was your process sound?” but “why didn’t you own more?” It means, in the specific silence that follows that question, having to defend a philosophy that has not yet been tested by the market conditions it was designed for.

Being right in a way that looks wrong is one of the hardest things in professional investing, and no framework eliminates that difficulty. The claim for risk-first sizing is narrower and more durable: it preserves the ability to compound by avoiding the drawdowns that force you out of the game. The most important position in a portfolio is the one you can actually hold. The most valuable returns are the ones you are still around to collect.

───

What would change this view?

The framework has two genuine vulnerabilities that the standard version of this discussion tends to understate.

The first concerns the stress scenarios that determine position sizes. The framework assumes these can be estimated with reasonable accuracy: that a forty per cent drawdown for a quality compounder is a credible adverse case rather than a floor. The evidence suggests that stress estimates are systematically too optimistic. In 2022, high-quality growth businesses that would have been stress-tested at thirty to forty per cent fell fifty to seventy per cent from their peaks. If the inputs to the loss budget are consistently underestimated, the positions produced by the arithmetic are consistently too large, and the protection is less effective than it appears. The methodology is sound. The estimates it depends on are not objective, and the direction of error in late-cycle markets is not random.

The second concerns institutional durability. Risk-first sizing requires commitment through periods of relative underperformance that most governance structures cannot sustain. A portfolio sized this way will, in most strong markets, trail a portfolio sized without these constraints. If that period extends for three or four years, which it can, the framework tends to be abandoned before the stress event that would have vindicated it. The most useful proof of risk-first sizing is visible only in the markets the framework was designed to survive. Those markets are infrequent, unpredictable, and arrive after the patience of most committees has already been exhausted.

A discipline that is discarded before it is tested provides less protection than one that is never adopted.

───

Sizing is the least glamorous part of portfolio construction. It does not generate ideas or identify opportunities. It cannot tell you which businesses will compound or which theses will prove correct. What it does is narrower and, across a complete cycle, more consequential: it determines whether the portfolio still exists when the ideas that were right finally prove themselves.

Hwang’s ideas didn’t need to be wrong. They needed to be late. A portfolio sized only for the case where it is right, and on time, is not risk management.

Downside sets size; expected return sets order. The right size always looks excessive before the market tests it, and obvious afterwards.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative and hypothetical. This material is intended for wholesale and professional investors.