The Paycheque That Buys the Market

Superannuation converts wages into market exposure by default. AI compresses the wages that feed contributions. It also concentrates the index those contributions buy. Both pressures are structural and already running.

15 min read | By the team at Banyantree Investment Group

Before code became invisible, it was punched by hand: rows of holes, binary made physical, logic expressed as labour. Card punch operator, c. mid-20th century. Source: National Archives and Records Administration (NARA). Cropped, redrawn, and colour-treated.

───

The superannuation contribution file arrives overnight.

It is an unlovely thing, the remittance advice that tells the fund which accounts to credit: a list of amounts and identifiers that looks more like plumbing than finance. On a good day it is perfectly dull. The totals reconcile, the cash lands, the system ticks over. In the morning, someone checks it with the same mild attention you give the weather. Not because it is interesting, but because it is there, every day, whether markets are calm or hysterical.

For years it changes the way rainfall changes, within a familiar band. Then, gradually, it does not.

The list is still long, still regular, still boring. But it is lighter in places you do not see in headlines. Headcount is down in quiet corners. Hours have become more elastic. A certain kind of corporate language grows sunnier: efficiency, leverage, productivity. The market calls it progress. The file calls it flows.

If you spend enough time around markets, you begin to notice that we talk about them as if they are arguments. Fundamentals versus narratives. Bulls versus bears. Value versus growth. But what keeps markets continuous is less philosophical than that. Someone, somewhere, has to keep showing up with cash: not once, but repeatedly, in numbers large enough to matter. Not because they are inspired. Because they are enrolled.

Australia has a particularly visible version of this enrolment. Superannuation is tied to wages and collected by default. It is not that every dollar ends up buying Australian shares. It does not. It is that an enormous, habitual flow is converted into investment exposure across portfolios, local and global, whether the underlying investor feels confident, tired, distracted, or simply busy living their life.

You can call it a system. You can call it a policy. In practice it behaves like a pipe.

And when a large pipe changes, the room changes with it.

───

Three quiet supports have started to shift at the same time. The Super Guarantee has reached its legislated ceiling of 12 per cent, so contribution growth now depends far more on wages and employment than on policy ratchets. White-collar employment growth has softened, and professional-services wage growth has cooled at the margin. Meanwhile the AI platforms that sit at the top of the index are pulling more weight, literally, inside benchmark-aware portfolios.

This is where AI enters the story. Not as a sector you pick, or a slogan you fear, but as a force operating simultaneously on both ends of the chain. From below, it threatens the wage income that feeds the file. From above, it concentrates the index that the file ultimately purchases. These are not separate arguments that happen to share a subject. They are two expressions of the same underlying transfer: economic value migrating from the broad labour income of the knowledge-work class to the narrow capital income of the platforms doing the displacing.

The mechanism is already running.

───

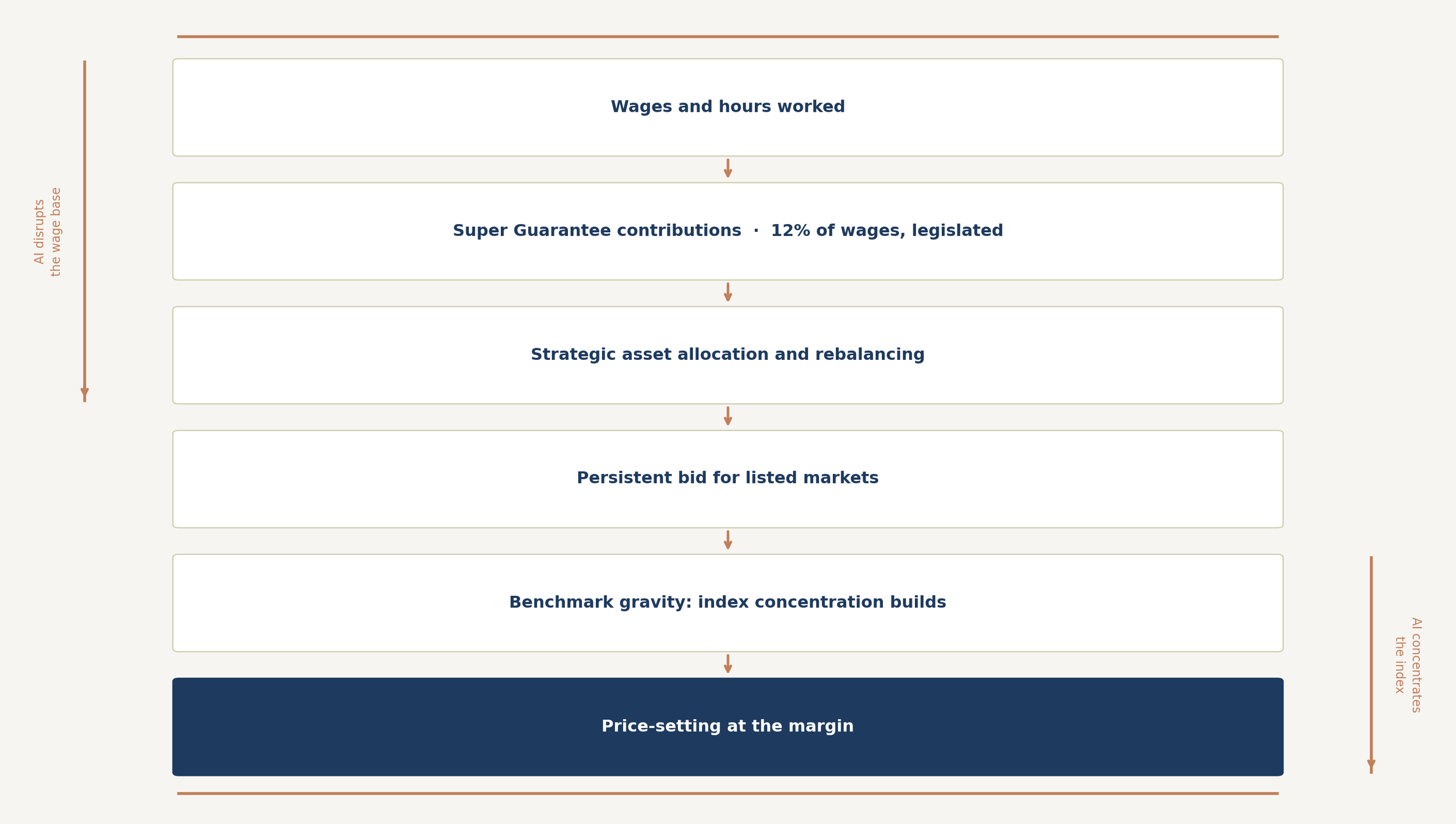

Exhibit 1 : From Paycheque to Price

The chain from wages to contributions to allocation to market prices, with AI operating simultaneously on the wage base at the left and the index composition at the right. Illustrative. Not personal advice.

───

"At the margin" is a phrase used in markets to describe something simple: prices are set by the next buyer, not the average one. The marginal buyer is not necessarily the largest pool of capital in the world. It is the buyer who shows up, reliably, when bids and offers meet. Change that buyer, or change how reliably they appear, and you can change market behaviour without changing the story people tell themselves.

There are two kinds of marginal buyer worth distinguishing. The trading marginal buyer sets prices on the day through liquidity, positioning, and market structure: visible, discussed, modelled. The allocation marginal buyer is slower, easier to miss, and far more powerful over months and years, because it supplies persistent net risk-bearing capacity. Superannuation flows are the allocation marginal buyer for Australian-listed assets. For global exposure, where the largest funds now hold forty to sixty per cent of growth assets internationally, the mechanism runs through different pipes. What follows is most legible for the domestic market, where the paycheque-to-price link is unusually clear.

Patience, in this context, is a structural condition: the ability to hold a long-duration, illiquid, or contrarian position without forced exit, because the portfolio has the background support to wait for a thesis to resolve. When the allocation marginal buyer is steady and diverse, patience is cheap. When it becomes variable or concentrated, patience becomes a premium. A portfolio that cannot fund that premium from somewhere else is forced to make decisions it would not otherwise choose.

APRA’s annual superannuation statistics for 2024–25 give the throughput plainly. Total contributions: A$209.4 billion. Benefit payments: A$132.2 billion. Net contribution flows: A$70.9 billion. Those are not decorative figures. They are the throughput of a machine that quietly converts wages into markets.

───

I. When work becomes less steady, investing becomes less steady

Consider a person in her forties. She has skills. She is, in the current language, augmented. Her job survives. But her life becomes a patchwork. A contract extension here. A retraining course there. Two gaps of three weeks between projects that are not called unemployment but feel like it. A second role picked up to smooth cashflow. Employment looks stable on paper. Income becomes spikier in real life. Saving becomes more defensive. Planning becomes more tentative. Contributions still happen, but they arrive in bursts.

Nothing dramatic needs to occur for the contribution file to change. Stability only needs to erode at the edges.

There is already evidence that those edges are eroding. White-collar employment in Australia grew by just 0.8 per cent in 2024–25, 43,900 workers, the slowest rate in a decade, according to Deloitte Access Economics. In the same period, the Wage Price Index for professional and financial services ranked among the softest sectors in the economy, lagging the national headline. A single year of softened growth is consistent with post-pandemic labour market normalisation following an unusually hot cycle, and that alternative deserves acknowledgement. What makes this reading more than noise is the coincidence of two structural changes arriving simultaneously: white-collar hiring cooling at precisely the moment the SG ratchet has switched off. These are not confirmations of the thesis. They are the thesis beginning to show itself in ordinary numbers.

There is a further structural pressure that receives almost no attention in investment commentary. The Super Guarantee rate reached its legislated ceiling of twelve per cent in July 2025. The decade-long tailwind that inflated employer contribution growth, successive annual rate increases that mechanically boosted inflows above the organic growth of wages and employment, is now spent. From this point, employer contributions grow only as fast as wages and employment grow. The engine that has been flattering the pipe’s organic growth rate is switched off.

The margin for patience narrows when net cashflow slows, and the structural tailwinds sustaining that cashflow have both run their course simultaneously. Millions of pay cycles blur into a steady-looking line at the system level, but the aggregation does not change what is underneath it. When inflows become variable or structurally softer, rebalancing constraints tighten, liquidity demands from benefit payments compete for the same cash, and the holding period for long-duration positions effectively compresses. In that world, the portfolio’s job is not only to compound. It is to remain coherent when the cash arrives unevenly.

───

II. When the file funds its own compression

There is a second process operating on the other end of the chain, running in the same direction as the first.

The contribution file does not choose what to buy. It moves through default allocations into balanced and growth options, most of which carry meaningful exposure to market-cap-weighted indices. Those indices, in turn, do not choose what to own. They own what is largest. And what is largest, in 2025, is a small number of technology platforms capturing the rental income of artificial intelligence.

As their market capitalisations grow, their weight in the index grows with them. The passive investor who believes they hold a diversified slice of the economy holds something materially different: a market-cap-weighted bet on the platforms capturing AI rents, surrounded by a diminishing tail of everything else. Their portfolio is diversified by name count. By risk source, it is concentrated.

What this means for a superannuation fund’s liquidity profile under stress is specific and worth naming. When the few companies dominating the index move together, as they do in stress, the diversification benefit of holding the index disappears at exactly the moment it is most needed. Redemptions and benefit payments still arrive on schedule. But the assets backing them are, in a stress scenario, behaving like a concentrated portfolio rather than the broad one the default allocation promised. The contribution file is funding this concentration quarter by quarter, one payroll cycle at a time, without any deliberate decision having been made.

The workers whose wages feed the pipe are also, through their default allocations, buying growing stakes in the companies replacing their tasks. The loop is not conspiratorial. The mechanism is clear, even if its magnitude and pace remain genuinely uncertain.

───

III. Who captures the gains decides who does the buying

AI may boost productivity. It may raise GDP. But productivity is not the same thing as broadly shared purchasing power.

If AI’s gains accrue disproportionately to capital owners, the bid shifts away from households. It does not vanish. It relocates. Corporate buybacks tend to be pro-cyclical: strongest when confidence is already high, weakest when caution is rational. Systematic strategies provide steady demand until the moment they become liquidity-sensitive, at which point they pull in the same direction as the market is already moving. Concentrated private wealth can be patient, but ownership narrows, and behaviour becomes more narrative-driven. The broad, wage-linked bid had a stabilising quality not because it was wise, but because it was habitual and diverse: it funded the market from millions of distinct economic circumstances simultaneously. When that diversity contracts, the remaining buyers share more assumptions, more exposures, and more reasons to move in the same direction at the same time.

This claim is debated, and it should be. Some economists argue that AI will complement skilled labour and widen the wage distribution upward. Others, notably Daron Acemoglu and colleagues, argue that the task-substitution effect for knowledge work is more likely to compress labour’s share than previous waves of automation, because AI targets the cognitive tasks that had previously sheltered the professional middle class. The honest position is that this is uncertain, and the outcome depends heavily on adoption speed, regulatory response, and the ability of labour markets to absorb displaced workers. What is not uncertain is the direction of the mechanism, even if its magnitude is unknown.

A thinner market is not necessarily a weaker market. It is a less forgiving one.

───

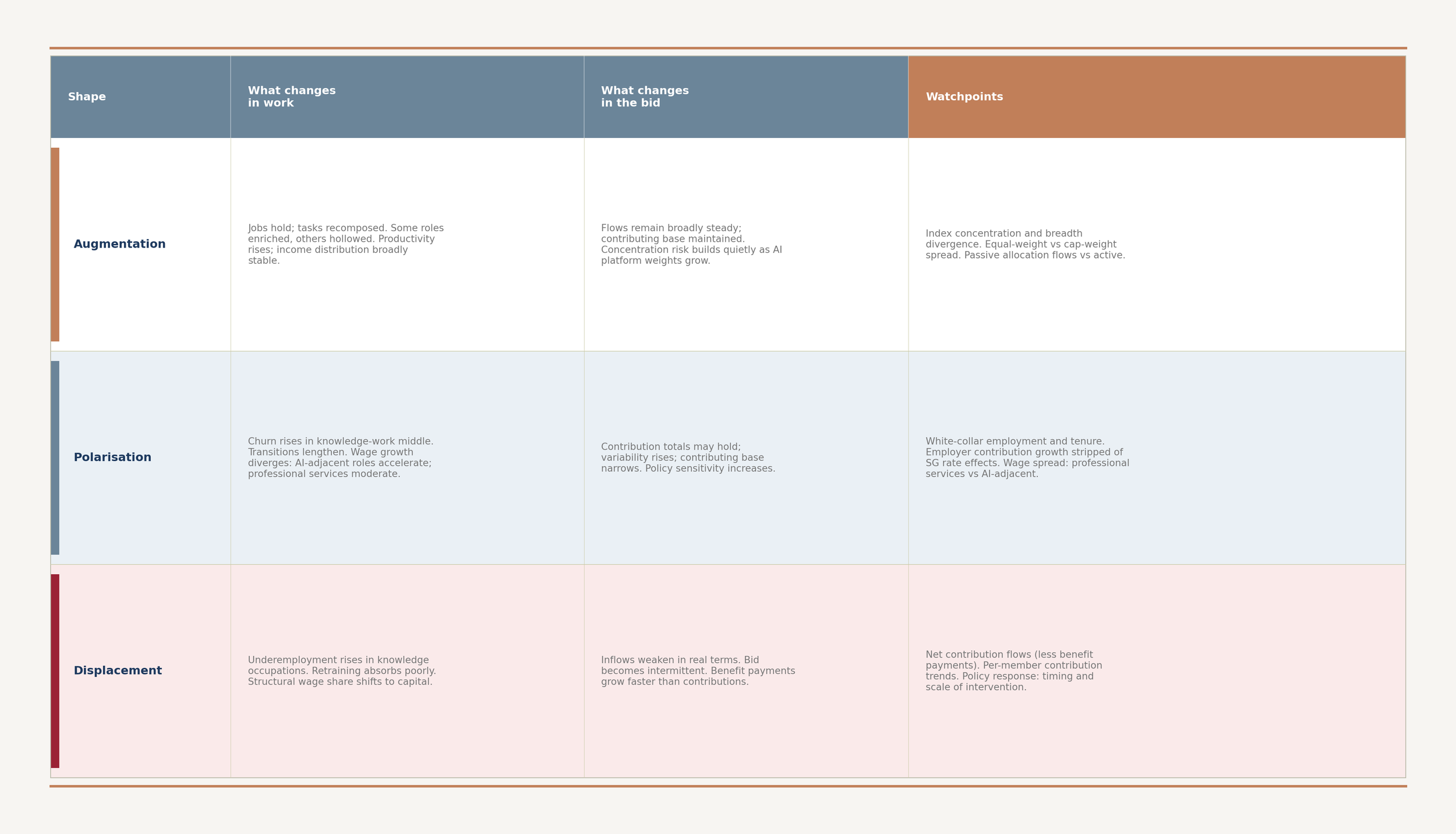

Exhibit 2 : Three Labour Shapes and Their Market Fingerprints

Three scenarios for AI's impact on labour: augmentation, polarisation, and displacement, with corresponding effects on contribution flows, index concentration, and the character of the marginal bid. Illustrative. Not personal advice.

───

What to Watch

The instruments that tell you whether the pipe is changing

If this thesis is right, these are the tells. Not market narratives, not conference chatter, but the small, repeatable measures that change before price does.

The most useful signals are not in equity markets. They are in labour market data, specifically in what is happening to employment stability, wage distribution, and churn in knowledge-intensive occupations. ABS Wage Price Index releases, read by sector rather than headline, show whether professional and financial services wages are tracking above or below the economy. Deloitte Access Economics employment forecasts track white-collar headcount growth. These are the early readings of a process that shows up in the contribution file years later. Aggregate unemployment is a lagging and politicised indicator. Sector-level wage growth and white-collar employment trends are not.

Superannuation contribution data provides the second instrument, and it requires a specific adjustment to be useful. Employer contribution growth has been inflated for a decade by successive SG rate increases. With the rate now at its legislated ceiling, any further growth in employer contributions reflects only wage growth and employment growth. Strip out the SG rate effect, which APRA’s quarterly releases allow, and you can see the organic growth rate of the pipe directly. A sustained deceleration in that organic rate, particularly if accompanied by acceleration in benefit payments as the retiree cohort expands, narrows the net flow that funds the market’s patience.

The third instrument is index concentration: specifically, the spread between equal-weight and cap-weight index returns. When this spread is wide and persistent, when the index is rising while most of its constituents are flat or falling, the structural buyer is increasingly funding a concentrated bet rather than broad participation. Advance/decline lines and sector dispersion tell the same story in different registers. A market where index and breadth diverge for an extended period is one where the assumptions embedded in passive allocation are most likely to be tested.

The fourth instrument is wage growth divergence between professional services and AI-adjacent occupations. If software engineers, AI researchers, and platform managers command accelerating wage premiums while junior lawyers, junior analysts, and junior accountants see wage growth moderate, in absolute terms and relative to their predecessors a decade earlier, that divergence is the earliest labour market signal that AI task substitution is operating in the knowledge-work cohort that funds the contribution file. It will not appear in a single ABS release. It requires watching the distribution, not the mean.

───

The contribution file will keep arriving. For a long time it may look exactly the same. It will still be boring. It will still be reconciliation and throughput and operational competence. In that sense, AI may not change it at all, not this year, perhaps not for several.

What AI may change is not the file’s appearance but the water table beneath it. The volume and steadiness of the rain. By the time the change is visible in the file, it has been operating in labour markets for years. By the time it is visible in labour markets, it has been operating in task composition and wage distribution for years before that.

The unsettling possibility is not that GDP falls. It is that GDP rises, that productivity improves, that corporate earnings grow, that the platforms at the top of the index compound beautifully, while the bid that has financed the market’s patience becomes narrower and less diverse. Markets have shown they can tolerate that divergence for a long time. What they cannot tolerate is the assumption that it is not occurring.

The first sign will not be in the price. It will be in the file, a little lighter in places that no one, at first, thinks to look.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative. This material is intended for wholesale and professional investors.