Every Style Is a Bet

A style label identifies what a manager buys. It also identifies who they are buying alongside. The crowd is not always visible until it tries to leave.

10 min read | By the team at Banyantree Investment Group

Every item in this room belongs to exactly one box. The system holds so long as nothing falls between the labels. Library catalogue room, c. 1917–1920. Library of Congress. Cropped, redrawn, and colour-treated.

───

On the morning of Tuesday, 7 August 2007, a quantitative equity fund at Goldman Sachs began losing money in a way its models could not explain. The positions were sound. The signals were intact. By the end of the week, the fund had lost close to a third of its value.

The event would have been unremarkable, just a bad week at a large fund, except for what was happening simultaneously elsewhere. Renaissance Technologies, run by the former codebreaker Jim Simons and widely considered the most successful hedge fund in history, was down nearly nine per cent in a strategy that rarely had losing months. Highbridge Statistical Opportunities fell around eighteen per cent. A dozen other quantitative funds were losing money in the same pattern, on the same days, in the same sequence, using systems built independently, in separate cities, by separate teams.

None of this should have been possible. Each fund was designed to be market-neutral: equal long and short positions, insulated from broad market swings. The S&P 500 barely moved on Tuesday and Wednesday. Whatever was happening was happening only to the quants.

Andrew Lo, a finance professor at MIT, later reconstructed the week using transaction data. His conclusion was precise and unsettling. The funds had independently converged on the same positions. The same value signals. The same momentum indicators. The same factor exposures. When one large player began liquidating, probably to meet margin calls from losses elsewhere, it moved prices against everyone holding the same trades. Those moves triggered further selling, which triggered further losses, which triggered more selling still. Goldman’s chief financial officer, in a moment of unusual candour, said the crowded trade had overwhelmed market fundamentals.

The analysis was correct. The thesis was intact. What had failed was the assumption each fund had made: that its exposure was its own.

───

The investment industry built its sorting system for reasons that made sense. Committees needed a vocabulary for allocating across managers. Consultants needed a framework for comparing them. Regulators needed a basis for disclosure. So the boxes were drawn: value, growth, quality, momentum, low volatility. Each resting on a body of academic research. Fama and French documented the value premium. Jegadeesh and Titman documented momentum. Novy-Marx documented profitability. The labels had genuine intellectual foundations.

The problem was not the research. The problem was what the labels did to portfolios once they were applied.

A manager hired to run a value strategy carries an implicit promise: this portfolio will behave like value. That promise has a cost. When value underperforms for two years, then three, then five, the committee faces the question it is required to ask: why are we paying active fees for this? The manager, under that pressure, adjusts. A growth name here. A momentum tilt there. Each change is individually defensible. Performance stabilises. The label does not change. The committee, reviewing a portfolio that now looks nothing like the value exposure they thought they had purchased, discovers the problem at exactly the moment when they can least afford to find it.

This is style drift, and it is one of the most reliable failure patterns in professionally managed portfolios. But drift is a secondary problem. The primary failure is more structural.

───

For fifteen consecutive years, from 1991 through 2005, Bill Miller’s Legg Mason Value Trust beat the S&P 500. It was the longest such streak on record. Assets grew to twenty-one billion dollars. The fund became, in the financial press, the canonical example of disciplined stock-picking.

The fund was called Value Trust. But it did not look like a value fund. Miller owned Amazon when most value managers considered it uninvestable. He owned Google shortly after its IPO. He built a heavy position in financials, including Countrywide, AIG, and Bear Stearns, on the thesis that their risks were misunderstood and their prices were cheap.

In 2008, Value Trust lost fifty-five per cent. The S&P 500 lost thirty-seven. The gap, eighteen additional percentage points of loss in the year clients could least afford it, ended the conversation. Redemptions followed. Assets fell from twenty-one billion to less than three. Miller stepped down in 2012.

What did the clients think they had bought?

The failures here were distinct and deserve to be named separately. The committee’s failure was accepting a label as a substitute for understanding what the portfolio actually held. Miller’s failure was allowing that misapprehension to stand: presenting the fund under a name that no longer described its contents. One is a governance failure. The other is a conduct failure. Neither excuses the other.

───

Style-neutral positioning is not an absence of views. It is a refusal to let a label dictate which views are permitted.

A style-committed portfolio starts with a category. We are value investors. Which stocks fit our criteria? The label arrives first; holdings follow. What gets excluded is determined not only by the analysis but by whether the analysis points in the direction the label allows.

Take the kind of situation that appears in a specific corner of Japanese industrials. A business trading at a slight premium to its five-year average on most conventional screens: expensive enough to be passed over by value managers. Earnings growth has been flat for three years, which removes it from growth consideration. The share price has underperformed the sector for six months, removing it from momentum strategies. On paper, it belongs in no box.

But the business completed a five-year restructuring eighteen months ago. The first external CEO in its history took the role shortly after. Working capital has been reduced by a third. Operating leverage is substantial: a modest volume recovery translates, in this business model, to a disproportionate improvement in margins and returns. The apparent expensiveness is an artefact of depressed earnings, not a premium on good ones. The restructuring is already done, not still being promised.

This kind of situation is not unusual. Businesses that fall between style definitions appear in every market at any given time. A style-committed manager, of almost any stripe, never reviews this company. The screens eliminate it before the analysis begins. A style-neutral manager asks whether the thesis is sound, whether the position can be sized safely, and whether the expected return is adequate. The label is irrelevant to both the question and the answer.

───

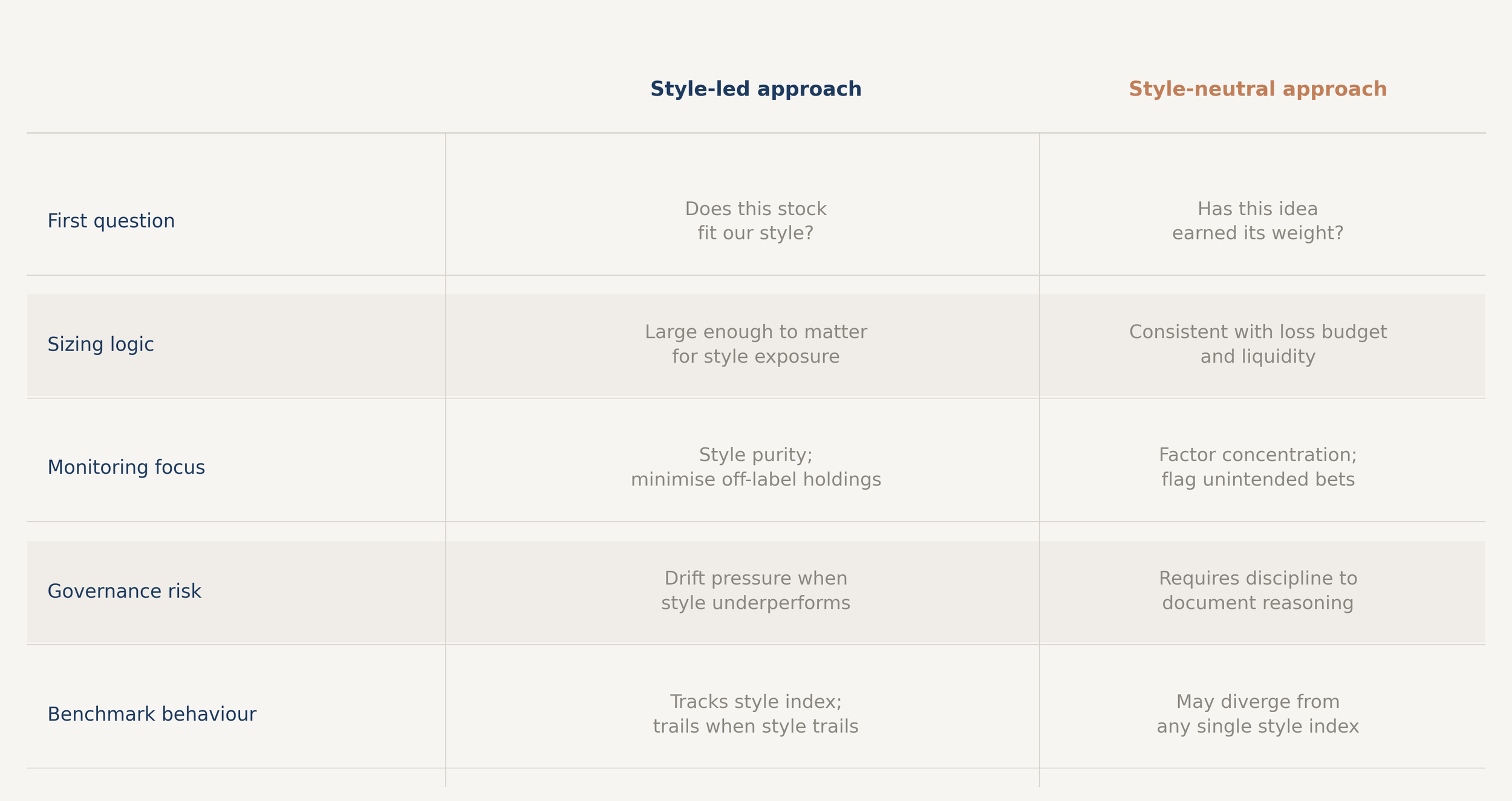

Exhibit 1 : Same Portfolio, Two Starting Questions

The same opportunity set evaluated under a style-committed framework and a style-neutral one. The holdings available for consideration differ by starting question. Hypothetical. Illustrative only. Not personal advice.

Once positions are selected, factor and style exposures become a monitoring exercise, not a design constraint. Every portfolio has a factor profile; that profile should be measured, reported, and reviewed. The governance question is not whether the profile fits a label. It is whether the profile reflects deliberate bottom-up decisions or has drifted into an unintended concentration. A dominant factor bet is still a bet, even if nobody decided to make it. The quants in August 2007 each believed their exposure was distinct. It was not. Style-neutral discipline does not guarantee convergence never happens. But it means the exposure was examined, rather than assumed to be unique because it carried a different name.

───

None of this removes the difficulty of looking different. A style-neutral portfolio will trail whichever style is leading at any given moment. When value surges, the portfolio has less value exposure than a pure value fund. When growth dominates, it has less growth exposure than a growth fund. The committee will ask why the portfolio does not look more like whatever is working. The manager will explain, again, that the goal is not to maximise exposure to the current winner but to avoid the hidden concentration that tends to resolve itself at the worst possible time.

The explanation is correct, but it is not comfortable. Comfort comes from conformity, and style neutrality is a deliberate refusal to conform to a single factor. The discomfort is the price of avoiding the larger risk: invisible convergence, crowded positioning, the next August 2007.

───

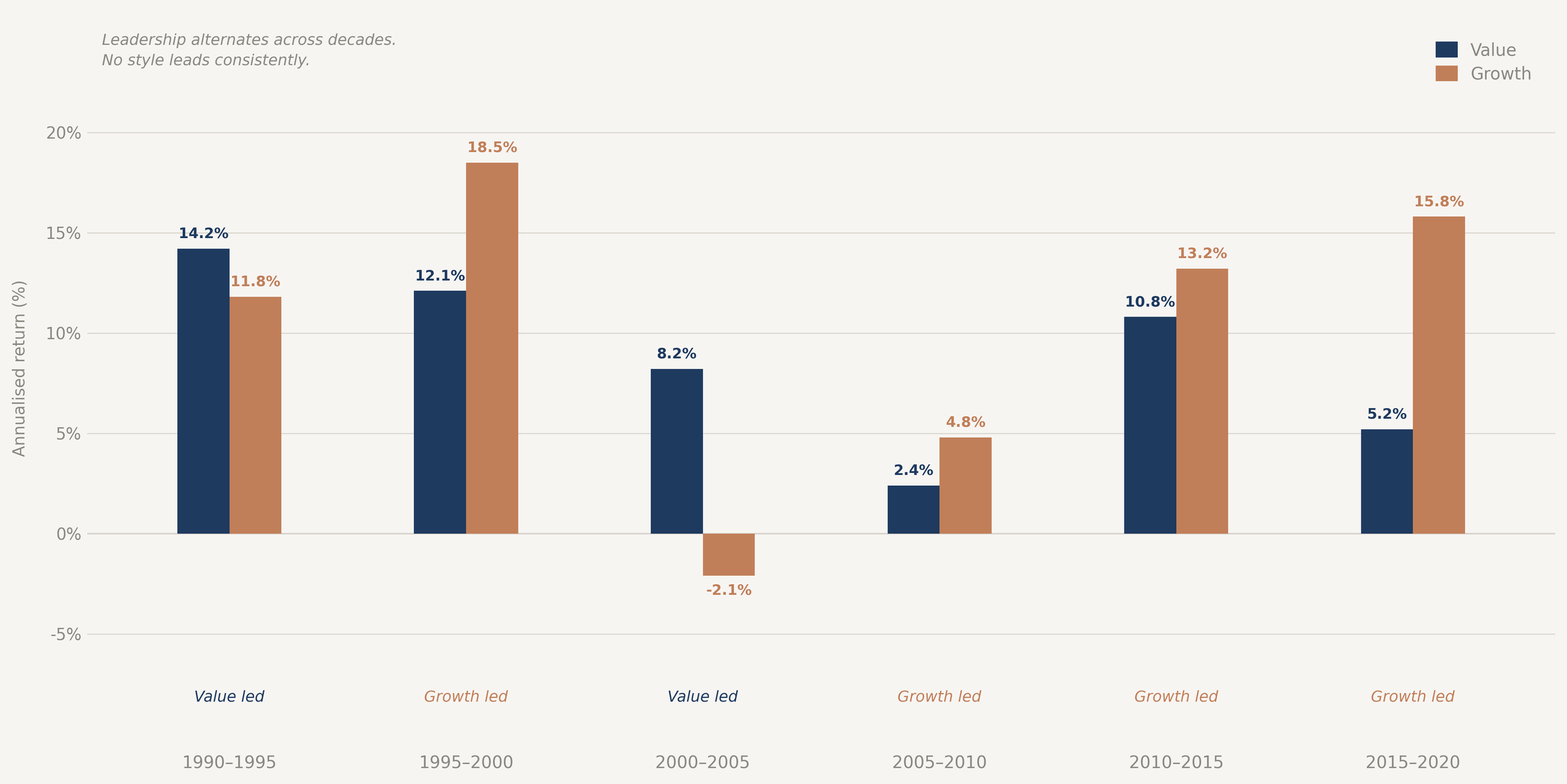

Exhibit 2 : Style Leadership Rotates

Illustrative annualised returns for value and growth style indices across four five-year periods, 1990 to 2020. Neither style has led in consecutive periods. Past performance is not indicative of future performance.

Style leadership rotates, and the rotation is unpredictable in timing even where it is predictable in pattern. A portfolio built for one regime lags badly in another. The style-neutral approach accepts a permanent modest drag relative to whichever box is currently winning, in exchange for avoiding the periodic catastrophic drag from being heavily committed to the box that has stopped working.

───

What would change this view?

The honest answer is more uncomfortable than the usual version of this discussion allows.

The most serious challenge is structural: the continued growth of passive investing and smart-beta products. Large pools of capital now flow mechanically into factor-defined strategies. If those flows have become persistent enough to make certain factor exposures self-reinforcing, a style-neutral approach may leave permanent return on the table rather than merely cyclical return. Anyone who has watched mega-cap concentration compound through passive inflows for a decade has grounds to press on this. A manager who held no strong view on that concentration has, on that specific question, underperformed by staying neutral.

The counter-argument is not that this risk doesn’t exist. It is that committing to the bet that factor concentration will continue requires a confidence about the future that the 2007 quant episode should have made genuinely difficult to sustain. Hidden convergence does not announce itself. It reveals itself at the worst moment. The framework accepts the possibility of leaving cyclical return on the table in exchange for not discovering, too late, that a supposedly independent position was really just another version of the same crowded trade.

If evidence emerged that factor timing had become reliably forecastable with the consistency required for real-world governance, the argument would weaken substantially. That evidence does not currently exist. If it did, the conclusion should change with it.

───

The quants who lost money in August 2007 were, by any reasonable measure, among the most sophisticated investors in the world. They had built systems that identified mispricings invisible to the human eye, exploited them with precision, and compounded returns for years. What they had not built was a way of knowing when everyone else had independently arrived at the same place.

Pick ideas, not lanes. Then watch your lane markers. The most dangerous assumption is that an exposure that appears distinct is yours alone.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative and hypothetical. This material is intended for wholesale and professional investors.