The Portfolio with Nothing in the Middle

The core is sized to survive. The ideas are sized to matter when the research is right. One risk budget governs both.

10 min read | By the team at Banyantree Investment Group

A reminder that measurement came before opinion: weight, counterweight, and the discipline of proving what something is worth. Byzantine steelyard balance, 5th–7th century CE. The Metropolitan Museum of Art, New York. Cropped, redrawn, and colour-treated.

───

For most of the previous decade, Universa Investments had been losing money.

The fund held deeply out-of-the-money put options: instruments that expired worthless in calm markets and had been doing so, quarter after quarter, since the fund’s founding. Universa paid a steady premium for the right to profit from catastrophe. When catastrophe failed to arrive, it paid the premium again. Some clients endured this patiently. Others concluded the approach was too costly to sustain and moved their capital elsewhere.

In March 2020, the S&P 500 fell thirty-four per cent in twenty-three trading days. Liquidity vanished. Correlations rose toward one. Portfolios that had appeared diversified revealed themselves to be variations on the same trade. On 7 April, Mark Spitznagel sent his remaining clients a letter.

The return for the quarter: 4,144 per cent.

───

The story is not about a fund that bet against markets and won. Universa’s clients did not use it to position against equities. They used it to stay invested in them. A portfolio allocating 3.3 per cent to Universa and the remaining 96.7 per cent to the S&P 500 would have emerged from March 2020 unscathed, in a month when the equity benchmark fell more than twelve per cent. Over the decade through early 2020, that combination compounded at 12.3 per cent annually, ahead of both the index alone and portfolios hedged with bonds or gold.

The structure behind this had a name. Nassim Taleb, who served as Universa’s scientific adviser, called it the barbell.

───

The barbell is not an allocation. It is a design principle.

Two extremes, nothing in the middle. One end holds positions designed to survive a wide range of outcomes, including those that cannot be predicted. The other holds positions with asymmetric payoffs, where the upside is large relative to the downside accepted. What gets deliberately avoided is the middle: the zone of apparently moderate risk that conceals fragility precisely because it appears sensible.

The logic is about the limits of knowledge, not about temperament. Risks at the tails of a distribution are genuinely difficult to estimate. A portfolio built entirely from middle-ground positions is exposed to errors in those estimates, and the errors tend to manifest at the worst moments. A barbell clips the downside by design. The core cannot lose more than its modest expected return. The ideas can lose only what was allocated to them. The combination produces what Taleb called antifragility: a structure that benefits from volatility rather than being destroyed by it.

A durable core provides the stability that allows a portfolio to remain invested through stress. A smaller allocation to high-conviction ideas provides the asymmetry that moves the needle when the research is right. Neither works alone. Core without ideas compounds slowly while the world changes around it. Ideas without core become concentrated bets with no margin for error. The barbell is what allows both to coexist.

───

Stanley Druckenmiller built one of the most remarkable records in professional investing: thirty years of compounding at more than thirty per cent annually, no losing years. His philosophy rested on one principle. When the evidence is clear and the thesis is sound, size should follow conviction. His mentor George Soros reinforced the lesson in 1992. Druckenmiller proposed shorting the British pound using the full capital of the Quantum Fund. Soros was dismissive. The opportunity was clear enough, he said, to go to two hundred per cent. The trade netted more than a billion dollars in a single day.

But Druckenmiller also provided the cautionary tale, in the same career, from the same framework.

In January 2000, he had already sold his technology positions. He had judged the bubble correctly and moved on. Then he watched two portfolio managers inside his own fund continue to make money in stocks he had exited. The watching became intolerable. He bought back in. He later recalled that he might have missed the top of the dotcom bubble by an hour. The loss on that single trade: three billion dollars.

The same investor. The same framework. Two opposite outcomes.

In 1992, conviction had been earned through analysis and expressed through size. In 2000, the size came first and the reasoning followed, dressed up as conviction. The barbell had worked. The problem was the decision to override it.

“I already knew better,” Druckenmiller said afterward.

───

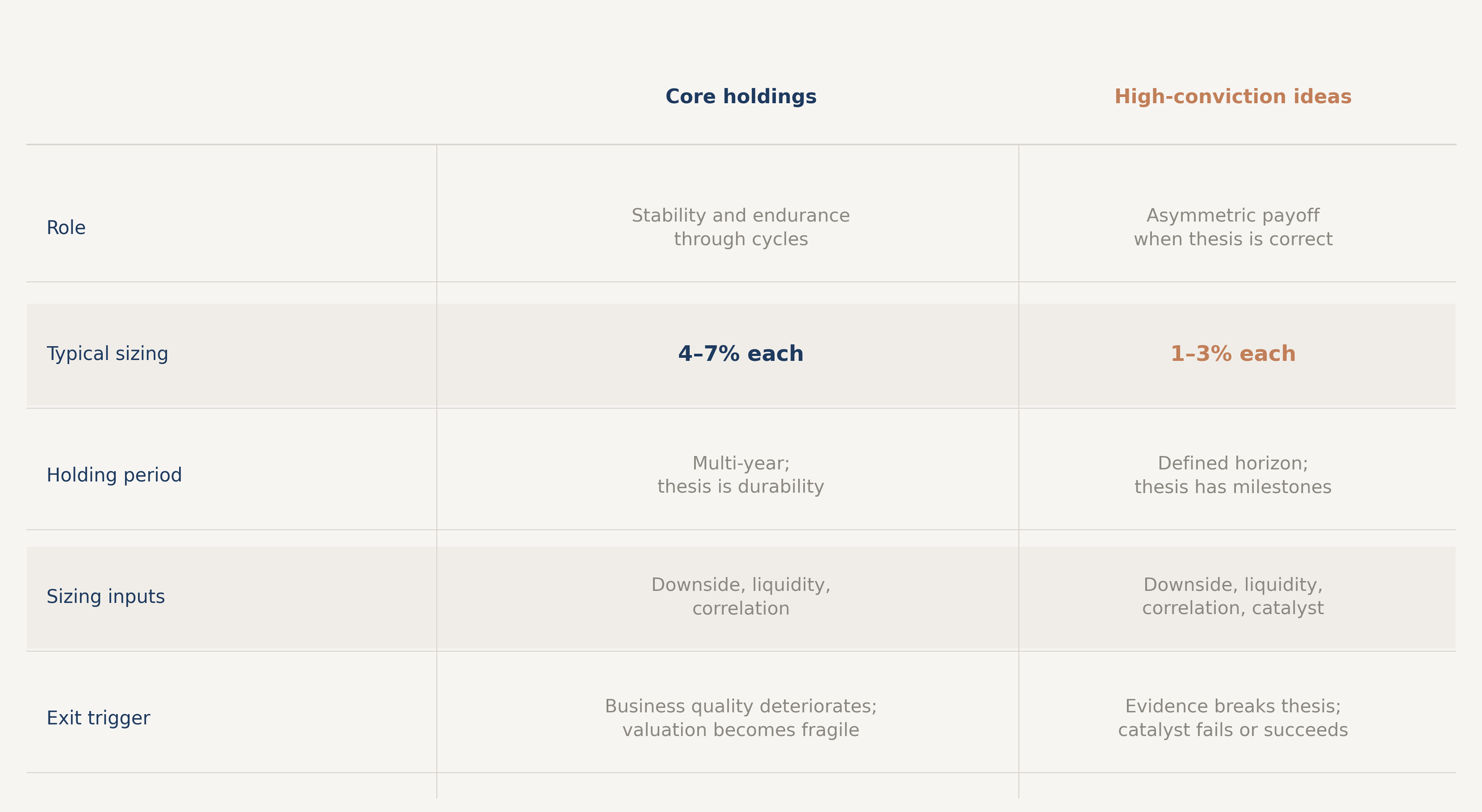

The first: what must be safe?

A core holding is not a familiar name or a large position. It is a position designed to be held through cycles, where the role is durability rather than return generation. Consider a regulated infrastructure business: long-dated contracted revenue, an investment-grade balance sheet, a demonstrated ability to sustain distributions through 2009 and 2020 without permanent impairment. The business is not cheap on conventional earnings metrics. It never is. Cheapness is not the test. The test is whether the position can remain in the portfolio through a thirty per cent market decline without forcing a sale, whether it provides income that reduces the portfolio’s dependence on capital growth in weak periods, and whether its behaviour under stress differs fundamentally from the positions on the other side. The answer in each case is yes. This is core.

The second: what is allowed to be opportunistic?

Consider a precision diagnostics business developing early cancer detection technology. Compelling clinical data, a specific regulatory decision expected within eighteen months that will either confirm or break the investment thesis. If the decision goes against the company, the position falls sixty to seventy per cent. If approval clears and the technology reaches commercial scale, the position doubles or triples. The expected value, given the clinical evidence, is genuinely attractive. But the outcome depends substantially on a single variable that analysis can inform and cannot determine. This position earns a weight of two per cent. Not because conviction is absent, but because the portfolio cannot absorb more in a severe stress scenario without breaching the loss budget. The size is the expression of the conviction, not its contradiction.

Both positions passed a valuation test and a sizing discipline. What differs is the role each plays. The infrastructure business is there to survive. The diagnostics business is there to generate an asymmetric return when the research proves out. Different expectations, different holding periods, one risk budget governing both.

───

Exhibit 1 : The Barbell Structure — Core Holdings and Ideas

A portfolio divided into a core allocation sized for durability and an ideas allocation sized for asymmetric return, governed by a single loss budget. Hypothetical. Illustrative only. Position sizes are indicative. Not personal advice

───

The barbell fails in predictable ways. Most of those failures begin with the same confusion: what looks like core is not.

A collection of large, popular, highly valued businesses can look like core in calm markets and behave like a leveraged bet in stress. Financial stocks in 2007 appeared core by every conventional measure: large, liquid, essential to the economy, generating stable dividends, trading at plausible valuations. They were not core in the sense that matters. They did not survive stress without permanent impairment. A portfolio manager who categorised them as core had not built a barbell. They had built concentrated exposure to a single risk, organised under the language of stability.

The ideas bucket fails differently. Deep research may correctly establish that a thesis is strong. The temptation is to size the position to match the strength of that belief. But conviction about the thesis is not certainty about the outcome. Sizing must still reflect downside, liquidity, and correlation with other holdings. A position can carry genuine conviction and still be capped at two per cent because the downside in a stress scenario is fifty per cent and the loss budget cannot absorb more. Sizing above that level is not the expression of conviction. It is the substitution of enthusiasm for arithmetic. Risk is controlled by sizing. Conviction is expressed through research.

Sizing discipline within a position is not enough if the positions themselves share the same underlying bet. Three positions in different sectors, at different valuations, can still depend on the same interest rate trajectory, commodity price, or regulatory outcome. Three costumes on one idea is not diversification. It is hidden concentration, which is why factor and theme exposure must be monitored across the ideas bucket, not only within individual positions.

What prevents all of this from accumulating unnoticed is pre-commitment. Without written criteria for when a position is resized or exited, ideas become permanent residents. The barbell dissolves slowly into a collection of positions that were once opportunistic and have since become simply held. Pre-commitment means writing down, before the position is taken, what evidence would confirm the thesis, what evidence would break it, and what valuation move would trigger resizing. This is what makes the ideas bucket auditable rather than improvisational.

───

Exhibit 2 : Two Buckets, One Risk Budget

Core and ideas positions with distinct sizing rules and expected holding periods, each constrained by a single shared loss budget. Illustrative only. Not personal advice.

───

What would change this view?

The most serious challenge is not about the barbell’s structure. It is about the judgement required to use it.

The framework depends on the ability to distinguish, with reasonable confidence, what belongs in the core and what belongs in the ideas. The financial stocks of 2007 showed how that judgement can fail systematically across an entire industry at once. Every portfolio manager had categorised them as core. No single decision was obviously wrong in isolation; the logic for each individual position was coherent. The aggregate was a catastrophe. The barbell is only as strong as the accuracy of the classification. If that judgement is systematically wrong, the structure does not protect against the error. It organises it.

The second challenge is correlation. The barbell’s logic assumes the core behaves differently from the ideas under stress. In March 2020, even Treasury markets became briefly difficult to transact at reasonable prices, and the distinction between safe and opportunistic compressed towards irrelevance for several days before recovering. A regime in which that compression became persistent, rather than temporary, would require a fundamentally different design. That regime has not arrived in the form that would overturn the framework. The risk that it might is real enough to require honest monitoring rather than comfortable reassurance.

The third challenge is liquidity. The barbell requires the ability to act on opportunistic positions without unacceptable cost: to trim, exit, or reweight when the facts change. If markets become so illiquid that ideas cannot be managed when the evidence shifts, the ideas bucket must shrink regardless of the quality of the thesis. Liquidity is not a background condition. It is part of the design.

These are not reasons to abandon the approach. They are reasons to hold it with specificity: to test, each year, whether what is labelled core would actually behave like core if the scenario arrived, whether the core still diversifies the ideas when stress appears, and whether the ideas can still be managed in the market conditions that exist rather than the ones the model prefers.

───

A barbell can look inconsistent. Stable holdings on one side, more aggressive positions on the other. Consistency lives in the structure, not in the individual positions. The core is there to survive. The ideas are there to perform. One provides the stability that allows the portfolio to remain invested through stress without forced selling. The other provides the asymmetry that moves the needle when the research proves out. Different roles, different sizing rules, one risk budget.

Druckenmiller built the structure and dismantled it in an afternoon in January 2000. Not because it had stopped working. Because watching others make money in his old positions had become intolerable. That specific failure, the dissolution of structure under social comparison rather than market pressure, is as reliable a risk as correlation rising in a crisis. The barbell provides no protection against it. Only the discipline to maintain it does.

Build the core to endure. Size the ideas to survive.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative and hypothetical. This material is intended for wholesale and professional investors.