What the Index Does Not Know

The benchmark tells you what the market owns. It does not tell you what anything is worth. Following it is often less about risk management than about career management.

12 min read | By the team at Banyantree Investment Group

The paths of the bodies inside this instrument were fixed before the demonstration began: mass, distance, and the laws that govern both. Joseph Wright of Derby, A Philosopher Giving a Lecture on the Orrery, 1766. Derby Museum and Art Gallery. Cropped, redrawn, and colour-treated.

───

The NASDAQ peaked on 10 March 2000. Twenty days later, Julian Robertson sent a letter to the investors of Tiger Management. He was closing the fund.

He had been right. Cisco, which Robertson had refused to own at a hundred and fifty times earnings, would eventually lose eighty-eight per cent of its value and take twenty-five years to recover its peak price. Yahoo, which he had declined to buy at valuations that required believing several impossible things simultaneously, would follow. The fund managers who had owned these companies on the way up would have explanations. Robertson would have been right.

He looked, in the language of the industry, ‘wrong’.

Tiger had been one of the most successful hedge funds in the world. Twenty-two billion dollars in assets. Two decades of disciplined returns. By early 2000, the capital was leaving. Robertson’s investors had spent two years watching peers discuss profits from companies he called uninvestable, and their patience had run its course. He was right. He was wrong on time. The NASDAQ would vindicate him within months. The fund was gone twenty days before it did.

What would you own if there were no benchmark?

───

In physics, gravitational pull is proportional to mass. The larger the object, the harder it is to escape its orbit. A stock that rises becomes a larger index weight, which means underweighting it costs more career risk, which means more managers avoid underweighting it, which means more capital flows toward it, which increases its weight further. The pull is not a one-time force to overcome. It is a continuous field, growing stronger the longer the divergence persists.

A global equity strategy, underweight the largest and most expensive benchmark names on valuation grounds, three quarters into a period of relative underperformance. Someone asks, politely, the question that echoes across the industry: why don’t we look more like this? Another notes that tracking error is elevated, the word chosen carefully, as though divergence from the index were a fever requiring diagnosis. The portfolio manager explains the rationale: valuation concerns in the largest constituents, concentration risk, liquidity under stress. The explanation is correct. In that room, it is also inadequate. Nobody demands the manager hug the index. They simply keep asking why the portfolio looks different, until it doesn’t.

This is how careers end without anything going obviously wrong. The manager capitulates gradually, not in a single dramatic decision but through a series of small adjustments, each individually defensible, none announced as a change of philosophy. The portfolio drifts toward the index. The manager, relieved, calls it risk management.

The asymmetry driving this is brutal. Bold and wrong ends careers. Timid and mediocre extends them.

Research from State Street’s Center for Applied Research, surveying two hundred institutional investors across endowments, foundations, pensions, and sovereign wealth funds, found the majority cited career risk as the single largest determinant in their decision-making. Not market risk. Not liquidity risk. Career risk. A manager who underperforms the benchmark by four percentage points while everyone else underperforms by three faces uncomfortable questions. A manager who underperforms by three alongside everyone else faces sympathy. The mathematics of career survival favour conformity, even when conformity means owning assets at prices that make no sense.

In early 2000, this is why so many professional investors owned Cisco at a hundred and fifty times earnings. They knew the valuation was untethered from any reasonable expectation of future cash flows. They owned it anyway. Being underweight a four per cent benchmark position that keeps rising is a career problem. Being wrong together is not.

───

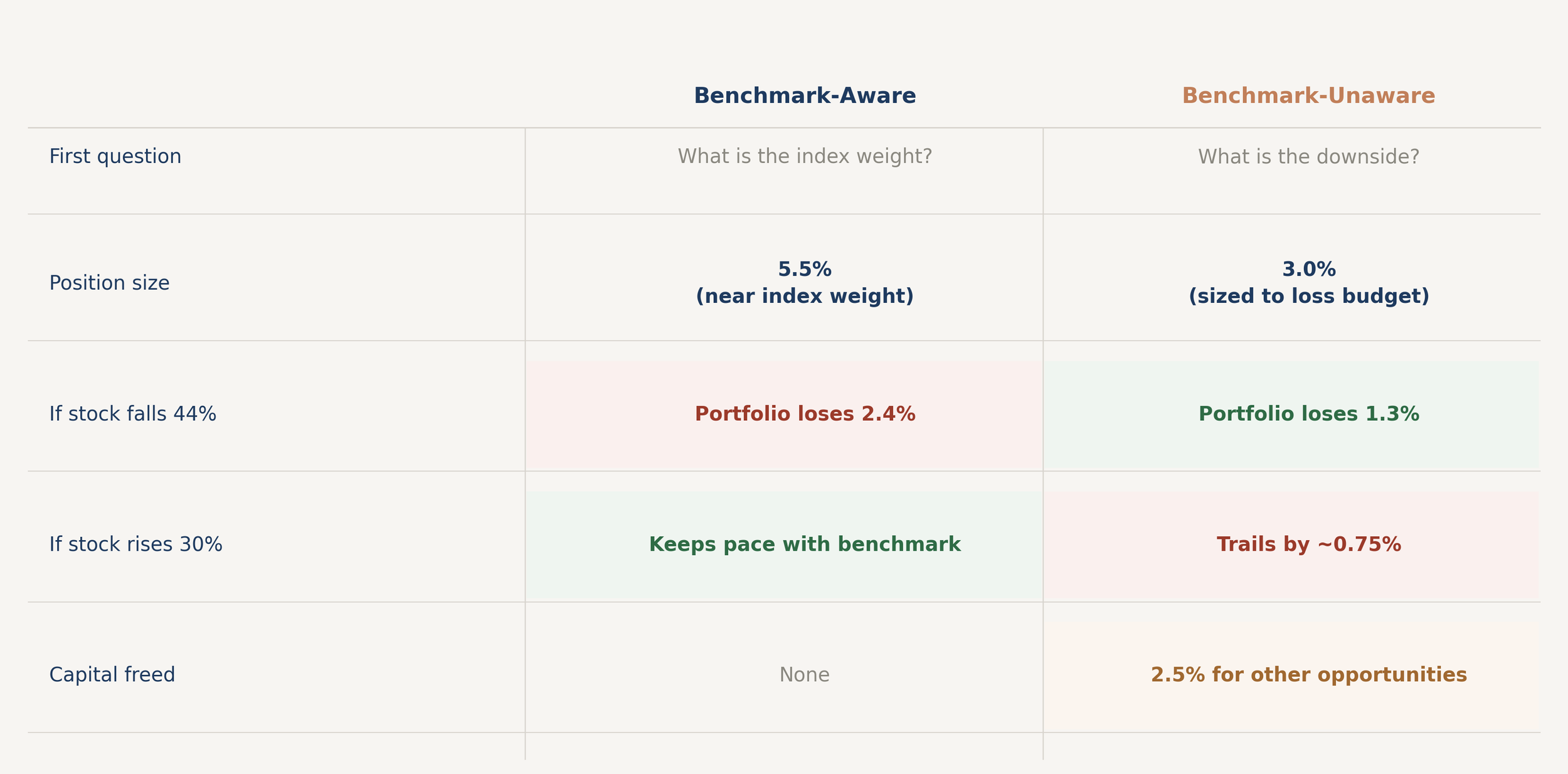

Consider what this calculus looks like on a specific name.

In the years following the pandemic, Microsoft grew to represent roughly six per cent of the S&P 500 and a similar weight in major global equity benchmarks. The business was, by almost any measure, exceptional: cloud infrastructure compounding at scale, recurring revenue, expanding margins, a competitive position rivals had repeatedly failed to dislodge. At various points between 2021 and 2023, the stock traded between twenty-eight and thirty-five times forward earnings, a level that embedded significant growth assumptions and left limited margin for disappointment.

A manager running a global mandate faced a specific decision. Underweight Microsoft by three percentage points, a meaningful divergence but hardly extreme, and if the stock rose another twenty per cent, that single underweight cost roughly sixty basis points of relative performance. Do the same with two or three similar benchmark heavyweights and a year’s relative return is explained before a single holding has done anything wrong. The gravitational calculus is straightforward: stay close, absorb a modest valuation discount, protect the seat.

The alternative question is harder. What does a six per cent allocation to this business, at this price, mean for the portfolio’s downside? Multiple compression from thirty times to twenty times earnings, combined with a modest earnings revision in a difficult environment, implies a drawdown of roughly forty per cent. At benchmark weight, this single name could cost the portfolio more than two percentage points in a bad year, before accounting for other high-quality growth holdings likely to fall alongside it. A manager who sized to benchmark weight was not taking a considered position on Microsoft. They were taking a considered position on their own quarterly review.

Starting from the portfolio’s mandate, loss budget, and actual view on the business produces a different answer. The weight that makes sense for the portfolio, given valuation, downside risk, and available alternatives, might be three per cent or four per cent or zero. The benchmark weight is a data point, not a directive.

───

Exhibit 1 : Same Stock, Two Frameworks

The same holding sized under a benchmark-driven framework and a risk-first framework. The starting question differs; the position sizes do too. Hypothetical. Illustrative only. Not personal advice.

The trade-off is explicit. If Microsoft rose another thirty per cent from an underweight position, the subsequent committee meeting would be uncomfortable. The right question in that meeting is whether the decision was consistent with mandate, valuation, and loss budget. That is a conversation about process, not a conversation about why the portfolio failed to orbit the same centre as everyone else.

───

Refusing to let a benchmark dictate decisions is not the same as being indifferent to it. The second posture, declining to report against any reference point, ignoring the reasonable expectation that a manager can explain relative outcomes, makes oversight nearly impossible. Against what would a committee measure results? A portfolio that cannot be evaluated cannot be trusted, regardless of the quality of the thinking behind it. A manager who cannot explain why the portfolio looks different from the index offers not independence but opacity.

The benchmark remains visible. It maps where the market is priced at a point in time, provides context, supports diagnosis, and makes relative performance explicable. What it does not provide is a list of holdings or a hierarchy of weights. The benchmark is the map. It is not the destination.

Loosening benchmark constraints without tightening everything else creates more risk, not less. If the index is not constraining the portfolio, the mandate and process must: documented reasoning, pre-committed signposts, explicit limits on divergence agreed before the divergence becomes uncomfortable. A stated philosophy of independence that becomes licence to drift is worse than a tight benchmark mandate. And if a committee cannot genuinely tolerate meaningful divergence over a multi-year horizon, it should not hire a manager who operates without one. That is not a criticism. It is clarity about what the arrangement requires from both sides.

Governance must be stronger when benchmark constraints are looser, not weaker.

───

Gravitational pull does not require anyone to act in bad faith. It operates through perfectly rational individual decisions that aggregate into a collective failure. The committee member who asks why the portfolio looks different is doing their job. The manager who gradually closes the gap to reduce the noise is managing career risk sensibly. The consultant who flags elevated tracking error is reading from the standard playbook. Each decision is locally defensible. The aggregate produces a portfolio that charges active fees and delivers passive outcomes.

This is closet indexing, and it is not as rare as the industry implies.

In 2015, the Norwegian Financial Supervisory Authority examined DNB Norge, the country’s largest fund manager. DNB had the lowest Active Share of any known collective investment fund in Europe, holdings so closely resembling the benchmark that it had virtually no chance of meaningfully outperforming it. Yet it charged active management fees. The regulator concluded DNB had failed to deliver the service its customers paid for. Norway’s Consumer Council filed a class action on behalf of 180,000 investors, seeking 690 million kroner in compensation.

DNB won at first instance. Oslo City Court ruled in January 2018 that the legal bar for compensation had not been met, even as the regulator had already found a breach of conduct obligations. Investors appealed. The Court of Appeal reversed that finding in May 2019. Norway’s Supreme Court upheld the reversal in February 2020, ordering DNB to repay approximately 350 million kroner. Think about the full sequence: a regulator found the product did not do what it claimed; a first court agreed the description was inaccurate but found no grounds for compensation; two higher courts overturned that finding; and five years after the original investigation, 180,000 investors received a partial refund of fees overpaid for a portfolio that had been orbiting the benchmark all along.

Research from ESMA found that between five and fifteen per cent of actively managed equity funds could be closet indexers. The UK’s Financial Conduct Authority forced managers to repay £34 million across sixty-four funds. The pattern is consistent across jurisdictions and decades: portfolios that charge for escape velocity and never leave orbit.

───

It would be dishonest to open with Robertson’s story and then avoid its implications. His fund faced redemptions rather than committee pressure, the mechanism was different from a long-only mandate governed by quarterly reviews, but the outcome was identical: capital withdrawn before the thesis was proved, at precisely the moment when patience had the highest expected value.

Relative returns can diverge for years. Not months or quarters, but the kind of multi-year stretches that outlast most oversight structures. Here is what that feels like from the inside. Quarter one: the portfolio trails. Commentary is measured. Positioning is intentional. Valuation discipline will be rewarded over the cycle. The committee nods. Quarter two: the gap widens. Can you walk us through the underweight in the largest benchmark names? The question is polite. The implication is not. Quarter three: an email arrives, not hostile, just a request for an updated note on how current positioning relates to the peer group. Peer group. By the fourth quarter, the conversation is no longer about the positions. It is about the manager. The committee is asking, in the silences between polite questions, whether they made a mistake hiring someone who doesn’t look like the index. Their own career risk is now entangled with the manager’s. Firing a manager who resembles the benchmark is difficult to justify. Keeping one who doesn’t is harder.

───

What would change this view?

Two conditions would require genuine reconsideration, and one of them is more uncomfortable than the standard version of this discussion allows.

The first concerns the continuing growth of passive investing. If passive inflows make large benchmark weights self-reinforcing through mechanical buying, underweighting the largest constituents may carry structural risk beyond the cyclical discomfort the Robertson story describes. This is not a settled empirical question, and a decade of watching mega-cap concentration compound through passive flows has given thoughtful sceptics reasonable grounds to press on it.

The second is more unsettling. The case for portfolio independence relies substantially on Active Share, the metric at the centre of both the DNB Norge case and most of the closet-indexing literature. Cremers and Petajisto’s original research linked high Active Share to outperformance, but subsequent work found the relationship sensitive to time period, fee level, and how the opportunity set is defined. If Active Share does not reliably predict what it is claimed to predict, then the quantitative foundation of the closet-indexing argument becomes difficult to defend.

Any manager operating without benchmark constraints should be able to answer a specific question: if Active Share turns out not to predict outperformance reliably, what does that mean for your approach? If the answer is “not much, because the underlying logic of valuation-based decision-making doesn’t depend on the metric,” that is a defensible position. If the answer is unclear, the objection has genuine force, and a committee pressing on it would not be wrong to do so.

───

Julian Robertson was right. He just wasn’t right on time.

The question that separates genuine active risk from a slightly eccentric version of the same trade is not whether a manager can explain the divergence. Any manager can explain it. The question is whether they can sustain it: when the benchmark is pulling hardest, when the committee is most uncomfortable, when the career-risk calculus most strongly favours giving in. That is the test. Robertson passed it. He ran out of investors before the market confirmed the score. The question was never the hard part. Holding the answer was.

What would you own if there were no benchmark?

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative. This material is intended for wholesale and professional investors.