The Architecture of Compounding

Magellan compounded. Its investors often did not. The difference was not the fund, but when they bought, sold, and doubted.

10 min read | By the team at Banyantree Investment Group

Sand moves in one direction and does not return. The frame is built to permit this and nothing else. Ornate sandglass, c. 1500–1525. The Metropolitan Museum of Art, New York. Cropped, redrawn, and colour-treated.

───

In the spring of 2014, Nick Sleep sent his last letter to the investors of the Nomad Investment Partnership.

He was forty-five years old.

The fund had returned 921 per cent since inception, against 116 per cent for the index. The investment cases were still intact, he wrote; the businesses could do the work without him. Not because markets were cheap. Not because he had a new thesis. He gave the money back.

The letters had always been typed in Courier: the font of a typewriter, chosen because it was not trying to impress. There were no pitch decks. The annual management fee was ten basis points, roughly one-tenth of the industry standard. At various points, Sleep and his partner Qais Zakaria had refunded fees when the fund fell short of its hurdle rate. New investors were required to sign a form acknowledging that the partnership was not suitable for anyone with a time horizon of less than five years. No other fund did this. They were, by design, making themselves difficult to own impatiently.

What they had built, behind the letters and the deliberate frugality of appearance, was a machine for preventing interruption. Not a machine for picking stocks, though they picked them well, but a machine for ensuring that the businesses they owned were given the time they needed to compound. The architecture of Nomad was the architecture of unbroken compounding: unleveraged, concentrated, evaluated over years rather than quarters, and built to hold.

The question worth sitting with is not why Sleep succeeded. It is why he had to build the machine so deliberately in the first place.

───

Between 1977 and 1990, Peter Lynch managed the Fidelity Magellan Fund to an annual return of 29.2 per cent, making it the best-performing mutual fund in the world. A dollar invested at the beginning of Lynch’s tenure and held through his retirement would have grown to something remarkable. The fund became famous. Magazine articles explained the method. Lynch published books. Magellan grew from eighteen million dollars in assets to fourteen billion.

A subsequent study by Fidelity found that the average investor in Magellan, over Lynch’s tenure, did not earn anything close to 29 per cent. By Lynch’s own account, the average investor made approximately 7 per cent annually.

The mechanism was simple: investors bought after strong years and sold after weak ones. They arrived at the fund when it appeared in glowing coverage, and they left during the quarters when it was uncomfortable. The fund compounded. They did not. The gap between the fund’s return and the investors’ return is the mathematical signature of interrupted compounding, and versions of it appear in every fund that has ever been measured. It is not a failure of intelligence. It is a failure of governance: the absence of a structure that protected investors’ processes from their own behaviour.

Sleep knew this. The five-year acknowledgement form was his answer. If you will not commit to the horizon the strategy requires, he was telling investors, you should not be in this fund. Not because your money is unwelcome, but because you will not benefit from it.

───

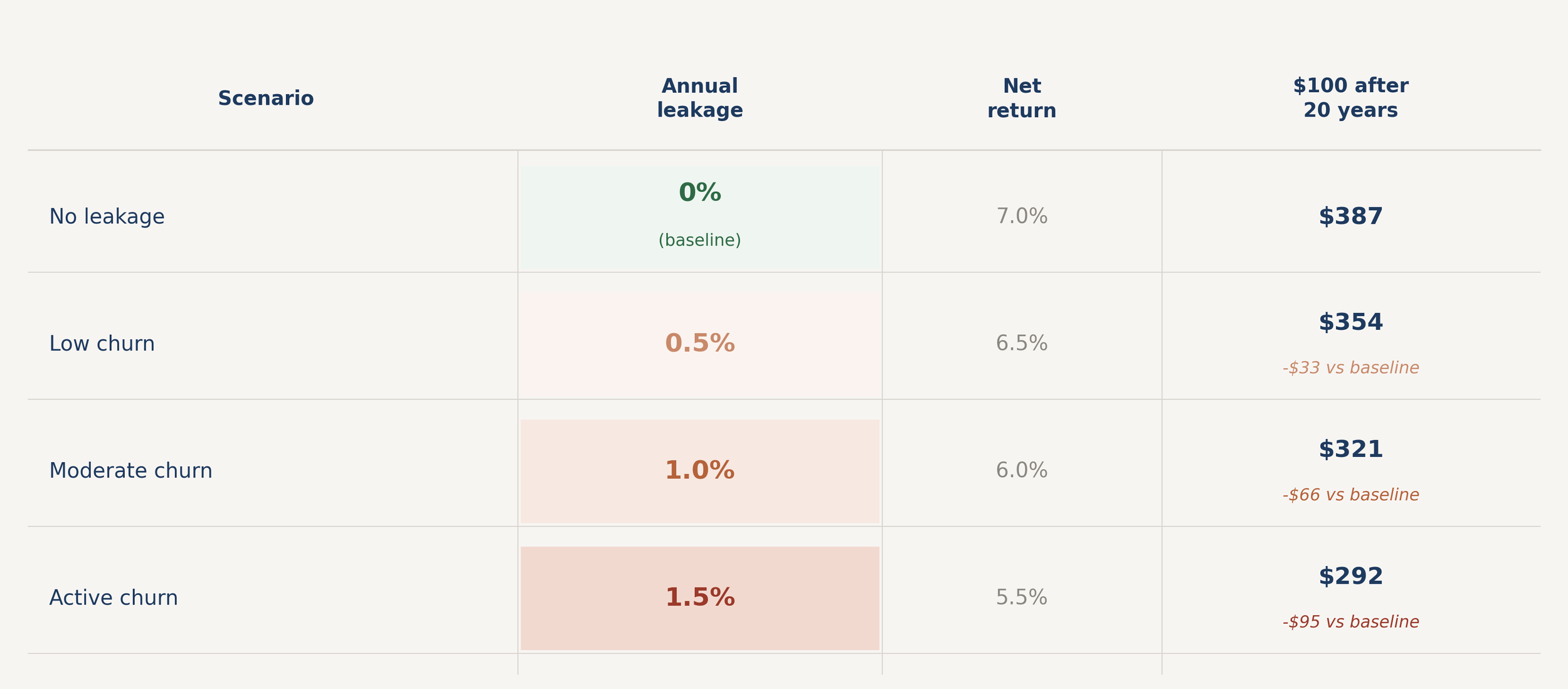

Exhibit 1 : The Cost of Leakage — Scenario Comparison

Terminal portfolio values compared across twenty years of clean compounding and compounding with one per cent annual leakage. Hypothetical. Illustrative only. Not personal advice.

───

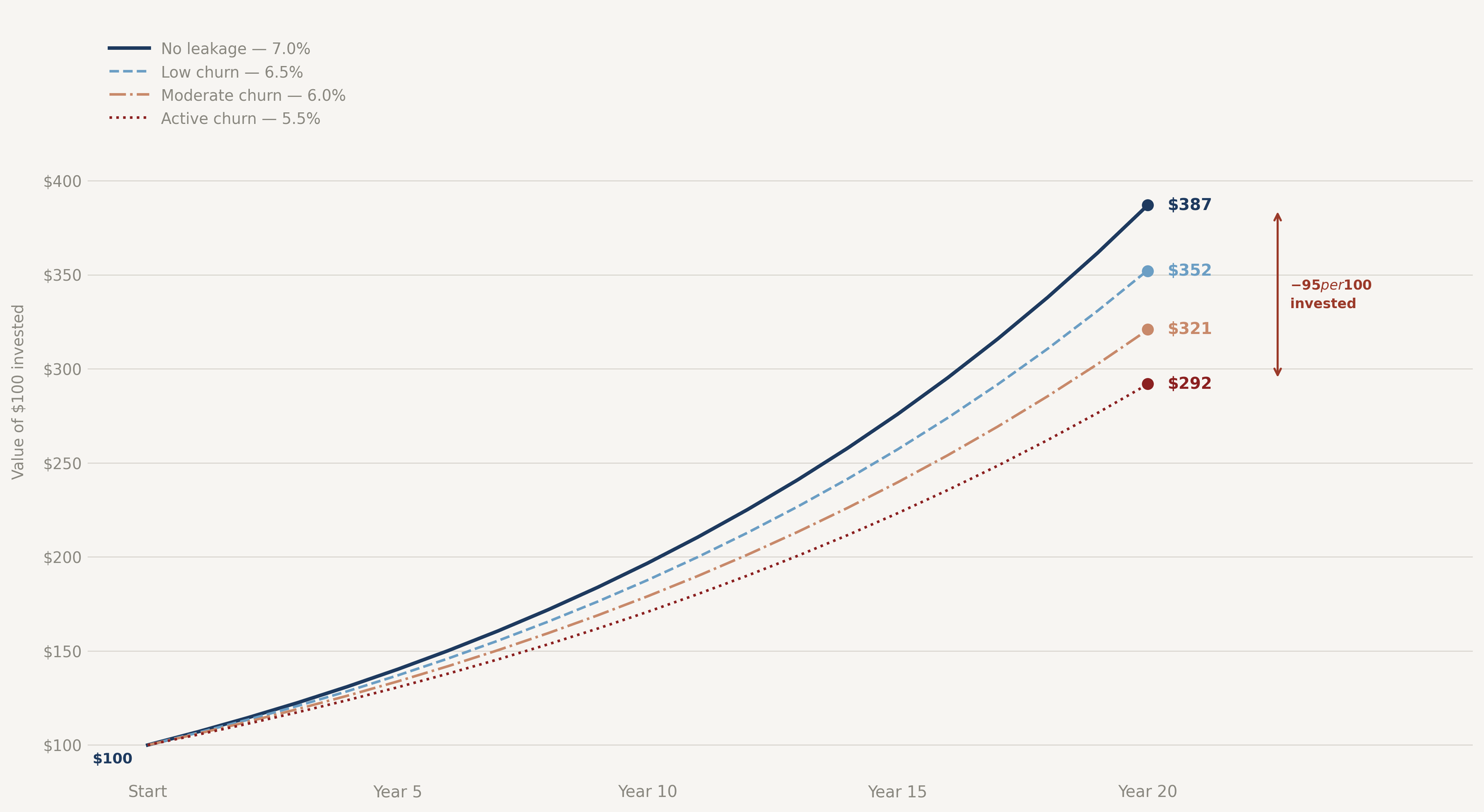

Exhibit 2 : How Leakage Compounds Over Time

Compounding paths at zero, half a per cent, one per cent, and two per cent annual leakage over twenty years. Hypothetical. Illustrative only. Not personal advice.

The numbers are not dramatic in any single year. Half a percentage point of leakage barely registers over twelve months. Over twenty years, one per cent of annual leakage costs sixty-six dollars for every hundred invested. The Magellan investors were not losing money to a single catastrophic decision. They were losing it to a pattern of small, socially sensible ones, each individually defensible, each compounding in reverse at precisely the same rate returns compound forward.

───

A quality-oriented strategy in late 2016, three quarters into underperformance against a benchmark that had surged on cheap cyclicals and resources stocks. The attribution report has a red column. A committee member, not hostile, not wrong, asks the reasonable question: is the process still working, or has something changed?

The chain most often breaks here: not in panic, but in a meeting. Not through a single catastrophic decision, but through a series of small, socially sensible ones. Someone suggests rotating into what has been working, just for now, just to reduce the noise. Someone else wonders whether a few visible trades would signal responsiveness. Each trade is defensible. Each costs a spread, a brokerage fee, a sliver of market impact. Together they create the pattern Magellan’s investors created: buying after re-rating, selling after drawdown, arriving late to each recovery. A trade should exist for one reason: valuation changed, risk changed, or the thesis changed. If none of those changed, activity is more likely to be self-soothing than value-adding.

That break is chosen. The next is not.

───

On 23 September 2022, the British government announced a fiscal package that included sweeping tax cuts financed by new debt. The bond market reacted with unusual speed. Gilt yields rose more than a hundred basis points in four days. The movement was sharp enough to expose a structural fragility that had been growing for years inside the UK’s defined-benefit pension system: liability-driven investment strategies, built to hedge long-duration liabilities, were leveraged against the very assets that were now falling. As yields rose, collateral calls arrived. To meet them, pension funds needed to sell assets quickly. The assets they could sell most quickly were gilts. Selling gilts pushed yields higher. Higher yields generated more calls. The loop had begun.

By the morning of 28 September, the Bank of England had concluded that without intervention, around ninety per cent of UK pension funds would exhaust their collateral by the end of the day. It committed up to £65 billion to purchase long-dated gilts. Estimates of total asset losses across UK pension schemes reached as high as £500 billion.

The managers doing the selling were not panicking. They were not abandoning their long-term views. In many cases the investment thesis was entirely intact. The structure made the decision for them. The collateral call did not care about the ten-year strategy. It required cash by 5 p.m.

The LDI episode demonstrates something the 2016 committee room does not: that behavioural discipline alone is insufficient. A portfolio built with excessive leverage, or with positions sized beyond what a client can hold through stress, will be forced to break its own chain regardless of the quality of its intentions. Position sizing to downside is a prerequisite for compounding, not a separate consideration. The portfolio that cannot survive stress cannot compound through it.

───

Churn is visible. Forced selling is audible. The third break leaves no evidence until it is complete.

By 1999, a value manager with a genuine decade of disciplined performance was facing a difficult situation. Three years of underperformance against a benchmark driven by technology stocks. The committee was asking questions. The quarterly meetings had a different texture. The adjustments came gradually. A software company framed as growth at a reasonable price because the switching costs looked durable. Lucent Technologies, bought on the way down at what looked like a discount to the replacement cost of its telecommunications infrastructure. A cable business justified as essential distribution rather than speculative growth. None of these moves was dishonest in isolation. Each was a genuine attempt to find value in a market that had moved away from conventional screens. Together they created something different: a portfolio that had quietly migrated toward the very exposures its manager thought he was avoiding. When the bubble burst in 2000, those positions did not act as hedges. They acted like what they were. By the middle of 2001, the fund had given back most of what the prior decade had built. The manager left shortly after.

Style drift is the most dangerous of the three breaks because it almost always arrives disguised as wisdom. Churn and forced selling are legible failures: you can see the trades, audit the collateral calls, trace the mechanism. Style drift looks like evolution until it does not. The compromises accumulate quietly, each one reasonable in isolation, until the mandate that clients hired is no longer the mandate being run.

Being unpopular is survivable. Being inconsistent is not.

───

By the time Nomad closed, the portfolio had contracted from eighteen positions at inception to three: Amazon, Costco, and Berkshire Hathaway. Not because Sleep had sold down his conviction in the other businesses, but because he had continued to find that these three were the clearest expressions of the compounding logic he was pursuing: businesses that grew by returning value to customers, creating the kind of durability that had more in common with physics than finance.

The dollar invested at Nomad’s inception was worth more than ten dollars by the fund’s close. The final letter suggested holding the remaining positions. The investment cases were still intact. Sleep was not predicting anything. He was describing a process that could survive his absence, that had been designed, from the Courier font to the unleveraged balance sheet, to resist every pressure the market would eventually generate.

───

What would change this view?

Two limitations deserve more than a dismissal.

The first: patience can disguise inaction as discipline, and there is no reliable way from outside a manager’s thinking to tell the difference. The five-year acknowledgement form addressed the investor side of the problem. It provides no governance mechanism for detecting whether the manager who has not traded in three years hasn’t traded because the process is working, or because they have stopped paying attention. A mandate built to prevent interruption must also contain explicit mechanisms for distinguishing the two. Most mandates of this kind do not. That is not a theoretical concern. It is the blind spot the architecture tends to create while solving for a different failure.

The second: the compounding thesis is strongest where competitive advantages are persistent, where the moats that generate returns today predict the moats that generate returns in five years. Amazon’s fulfilment infrastructure, Costco’s membership model, Berkshire’s capital allocation: these advantages took decades to build and remained legible across the period Sleep held them. The current environment poses a harder version of the question. Technology transitions in some sectors have compressed the half-life of advantage to the point where a five-year holding period may routinely outlast the specific quality it was bought to capture. The durability that justified the Nomad architecture in 2005 cannot be assumed in every opportunity set today. Identifying genuinely durable advantage is the hardest part of the process. It is not a solved problem.

───

Magellan’s investors made their worst decisions not during a crash but in the quiet periods just before and just after: arriving after a strong run, leaving during a rough patch. The UK pension schemes did not fail during a market they had prepared for; they failed during one they had assumed would not happen, because a leveraged structure leaves no room for assumptions to be wrong. The value managers who drifted in the late 1990s did not abandon their discipline in a single meeting. They adjusted it, repeatedly, in response to questions that seemed reasonable at the time.

In each case, the market itself was not the decisive variable. The decisive variable was the compounding architecture the investor had built, or failed to build, before the market arrived.

Compounding does not end in a crash. It ends in the series of sensible decisions that preceded one, often in the meeting just before.

───

General information only. Not personal advice. Past performance is not indicative of future performance. Examples are illustrative and hypothetical. This material is intended for wholesale and professional investors.